Business Interruption Insurance: How to Protect Your Revenue When You Can't Operate

Business interruption insurance replaces lost income when your business can't operate due to covered events—here's what it covers and why every business needs it.

BUSINESS INSURANCE

Felix | Pinoy General Insurance Services

2/20/20267 min read

Your restaurant catches fire. Insurance pays to repair the building and replace equipment. But what about the three months of lost revenue while you're closed for repairs?

That's where most business owners discover a devastating gap in their coverage: they have property insurance, but no business interruption insurance.

Business interruption (also called business income) insurance replaces lost revenue when your business can't operate due to a covered event. It's one of the most important—and most overlooked—coverages for small businesses.

At Pinoy General Insurance, we've seen businesses with excellent property coverage go bankrupt because they didn't have business interruption coverage. A fire or natural disaster didn't destroy them—the months of lost income did.

This guide explains exactly what business interruption insurance covers, how it works, what it costs, and why every Cerritos and Orange County business should have it.

What Is Business Interruption Insurance?

Business interruption insurance covers lost income and ongoing expenses when your business is forced to close temporarily due to a covered peril.

Covered perils typically include:

Fire

Windstorm

Hail

Vandalism

Theft (if the damage forces closure)

Water damage from burst pipes

Electrical or mechanical breakdown (with endorsement)

Not typically covered:

Pandemic or disease (special coverage required—see COVID-19 lessons below)

Floods (requires separate flood insurance + business interruption rider)

Earthquakes (requires separate earthquake coverage)

Power outages from external causes (unless you buy utility interruption coverage)

Government-ordered closures (unless specific endorsement)

What Business Interruption Insurance Covers

1. Lost Revenue (Net Income)

This is the primary purpose: replacing income you would have earned if the business hadn't been interrupted.

Calculation: Based on your historical financial records and projected revenue.

Example:

Your restaurant averages $50,000/month in revenue

Fire forces closure for 4 months

Business interruption insurance pays approximately $200,000 in lost revenue (after accounting for expenses you didn't incur)

2. Continuing Operating Expenses

Even when your business is closed, certain expenses continue:

Rent or mortgage payments

Employee salaries (if you keep paying them)

Utilities (electricity, water, internet)

Insurance premiums

Loan payments

Property taxes

Equipment leases

Business interruption insurance covers these ongoing costs during the closure.

3. Temporary Relocation Expenses

If you can operate from a temporary location while your primary location is repaired, the policy covers:

Temporary rent

Moving costs

Additional expenses to operate from the temporary location

Example: Your retail store floods. You rent a temporary space in a shopping center while repairs are made. Business interruption covers the temporary rent and moving costs.

4. Extra Expenses to Minimize Loss

Costs incurred to reduce the business interruption period:

Expedited equipment delivery

Overtime pay for faster repairs

Rental equipment

Temporary staffing

Example: You pay $10,000 extra for expedited delivery of replacement equipment, reducing your closure from 3 months to 1 month. The policy covers the $10,000 because it saved $100,000 in lost revenue.

5. Civil Authority Coverage

If government authorities force businesses in your area to close due to a covered peril (e.g., fire in adjacent building, gas leak, etc.), civil authority coverage pays for your lost income.

Important limitation: Most policies only cover 2-4 weeks of civil authority closures.

What Business Interruption Insurance Does NOT Cover

❌ Pandemic or communicable disease closures (unless you have specific pandemic coverage—rare and expensive)

❌ Voluntary closures (if you choose to close for renovations, that's not covered)

❌ Seasonal business fluctuations (normal revenue variations aren't covered)

❌ Loss of customers to competitors (if customers switch to competitors during your closure, lost future revenue isn't covered—only the interruption period)

❌ Physical damage to inventory (that's covered under property insurance, not business interruption)

How Business Interruption Insurance Works: A Real Example

Business: Cerritos restaurant, annual revenue $600,000 ($50,000/month average)

Incident: Kitchen fire caused by electrical malfunction

Damage: Kitchen destroyed, dining room smoke damage

Repair timeline: 4 months

Insurance coverage:

Commercial property insurance: $250,000 (covers repair costs)

Business interruption insurance: $300,000 limit, 12-month coverage period

What the business owner receives:

Property insurance payout: $180,000

Kitchen equipment replacement: $120,000

Dining room repairs: $60,000

Business interruption payout: $163,000

Lost net income: $120,000 (4 months × $30,000 net income/month)

Continuing expenses: $43,000 (rent, utilities, loan payments, insurance for 4 months)

Total insurance payout: $343,000

Out-of-pocket cost: $5,000 deductible

Without business interruption insurance:

Receives $180,000 for property repairs

Still owes rent, utilities, loans: $43,000

Lost income: $120,000

Total loss: $163,000 that insurance doesn't cover

Likely outcome: Business goes bankrupt, can't reopen

With business interruption insurance:

Repairs completed

Bills paid during closure

Employees retained

Business reopens successfully

How Much Business Interruption Coverage Do You Need?

Step 1: Calculate Your Monthly Net Income

Net income = Revenue - Variable expenses (costs that stop when you close)

Example:

Monthly revenue: $50,000

Variable expenses (inventory, hourly wages, supplies that stop when closed): $20,000

Monthly net income to cover: $30,000

Step 2: Calculate Continuing Fixed Expenses

Fixed expenses that continue during closure:

Rent: $5,000/month

Utilities: $800/month

Insurance: $1,200/month

Loan payments: $2,000/month

Salaried employees you keep paying: $4,000/month

Total fixed expenses: $13,000/month

Step 3: Determine Coverage Period

How long would it take to repair or rebuild your business location?

Typical estimates:

Minor damage (smoke, water, vandalism): 1-3 months

Major damage (fire, significant structural): 4-8 months

Total loss (complete rebuild): 9-18 months

Recommendation: Buy coverage for 12 months minimum. Most policies offer 6, 12, 18, or 24-month coverage periods.

Step 4: Calculate Total Coverage Needed

(Monthly net income + Monthly fixed expenses) × Coverage period

Example:

Monthly net income: $30,000

Monthly fixed expenses: $13,000

Coverage period: 12 months

Total business interruption coverage needed: $516,000

Step 5: Add Extra Expense Coverage

Consider adding 10-20% for extra expenses (expedited repairs, temporary location, etc.).

Final coverage recommendation: $550,000-$600,000

What Does Business Interruption Insurance Cost?

Cost varies significantly based on:

Industry (restaurants pay more than offices)

Revenue and coverage amount

Deductible (waiting period)

Building age and construction

Location and fire protection

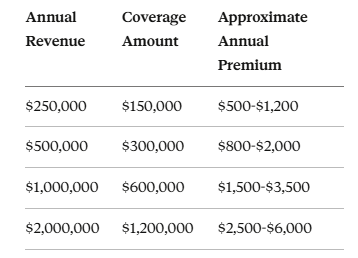

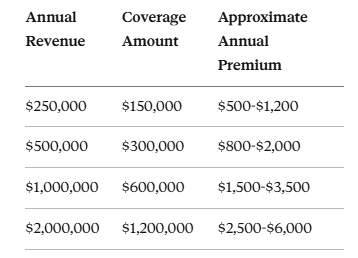

Average costs for California small businesses:

Cost as percentage of revenue: Typically 0.2-0.5% of annual revenue

Factors that reduce cost:

Higher waiting period (deductible)

Shorter coverage period

Sprinkler systems and fire suppression

Security systems

Updated electrical and plumbing

The Waiting Period (Deductible): How It Works

Unlike traditional deductibles (a dollar amount), business interruption policies have a waiting period—typically 48-72 hours.

How it works:

Coverage begins after the waiting period ends.

Example:

Fire occurs on Monday

Waiting period: 72 hours (3 days)

Coverage begins Thursday

If you reopen Friday (only 4 days closed), insurance pays 1 day of lost income

If you reopen in 2 months, insurance pays for approximately 59 days of lost income (60 days - 1 day waiting period)

Common waiting periods:

24 hours

48 hours (most common)

72 hours

7 days

Longer waiting periods = lower premiums

Strategy: If you can afford to cover 1-2 weeks of lost income from reserves, choose a 7-day waiting period to reduce premiums significantly (often 20-30% savings).

Industry-Specific Considerations

Restaurants and Food Service

High risk, high need:

Equipment-intensive (expensive to replace)

Perishable inventory

Health department inspections can delay reopening

Customer base may shift to competitors during closure

Recommendation: 12-18 months of coverage, include spoilage insurance and equipment breakdown

Retail Stores

Moderate risk:

Inventory can be stored temporarily

Seasonal businesses need coverage through peak seasons

E-commerce may allow some revenue continuity

Recommendation: 9-12 months of coverage, consider contingent business interruption (if suppliers are affected)

Professional Services (Law, Accounting, Consulting)

Lower risk:

Can often work from temporary locations

Less equipment-dependent

Client relationships may remain intact

Recommendation: 6-9 months of coverage, focus on civil authority and utility interruption coverage

Manufacturing

High risk, high need:

Equipment-intensive

Supply chain dependencies

Customer contracts may be lost

Specialized equipment has long lead times

Recommendation: 12-24 months of coverage, include contingent business interruption and extra expense coverage

Special Endorsements to Consider

1. Extra Expense Coverage

Pays for extraordinary costs to minimize business interruption—even if you don't fully close.

Example: Your HVAC system fails in July. You rent portable AC units for $3,000/month while waiting for repairs. Extra expense coverage pays for the rental units.

2. Contingent Business Interruption

Covers lost income if your supplier or key customer suffers a covered loss that interrupts your business.

Example: Your restaurant's primary food supplier has a warehouse fire and can't deliver for 6 weeks. You lose business because you can't get inventory. Contingent BI covers your lost income.

3. Civil Authority Coverage Extension

Standard policies cover 2-4 weeks of civil authority closures. This extends it to 8-12 weeks.

4. Utility Interruption Coverage

Covers lost income from power, water, gas, or telecommunications outages caused by damage to off-premises utility infrastructure.

Example: Power lines are damaged 2 miles from your business, causing a 5-day outage. Utility interruption covers your lost income.

5. Ordinance or Law Coverage

If new building codes require expensive upgrades when you rebuild, this covers the additional cost and extended business interruption period.

Lessons from COVID-19: The Pandemic Coverage Gap

The COVID-19 pandemic exposed a massive gap: most business interruption policies exclude pandemics and communicable diseases.

Thousands of businesses filed claims, believing they were covered. Most were denied because:

No physical damage to property occurred (business interruption requires physical loss)

Pandemics were explicitly excluded

Government closures weren't covered under civil authority provisions

What Changed After COVID-19:

New coverage options (limited and expensive):

Pandemic business interruption endorsements (rare, very expensive, limited coverage)

Parametric pandemic policies (pay a fixed amount if certain triggers occur)

What didn't change:

Standard business interruption policies still exclude pandemics

Most small businesses still can't afford pandemic coverage

Alternative strategies:

Build larger cash reserves (6-12 months operating expenses)

Develop business continuity plans that allow remote operation

Diversify revenue streams (e.g., restaurants adding delivery/takeout)

How to Buy Business Interruption Insurance

Step 1: Gather Financial Documents

You'll need:

Profit and loss statements (past 2-3 years)

Tax returns

List of fixed expenses

Revenue projections

Step 2: Calculate Your Coverage Need

Use the formula above to determine how much coverage you need and for what period.

Step 3: Get Quotes from Multiple Carriers

Business interruption is typically bundled with commercial property insurance (called a "Business Owners Policy" or BOP).

Shop at least 3 carriers:

Hartford

Travelers

Nationwide

Liberty Mutual

Chubb

Regional carriers

Or work with an independent agent who can quote multiple carriers simultaneously.

Step 4: Review Policy Terms Carefully

Not all business interruption policies are identical. Compare:

Covered perils

Waiting period

Coverage period (6, 12, 18, or 24 months)

Extra expense limits

Civil authority coverage

Exclusions

Step 5: Update Coverage Annually

Revenue, expenses, and business conditions change. Review and update your coverage every year to ensure it still meets your needs.

Red Flags: Signs Your Business Interruption Coverage Is Inadequate

❌ You haven't updated coverage in 3+ years

If your business has grown but your coverage hasn't, you're underinsured.

❌ Your coverage period is less than 9 months

Most business interruptions last 4-8 months. Six months of coverage may run out before you reopen.

❌ You don't have contingent business interruption

If you rely on a single supplier or key customer, their loss can interrupt your business.

❌ You have no extra expense coverage

Without this, you can't pay for expedited repairs or temporary operations.

❌ Your policy is based on outdated financial projections

If your policy calculates coverage based on 3-year-old revenue data, it's probably too low.

Final Thoughts

Business interruption insurance is the difference between a temporary setback and permanent closure.

Property insurance rebuilds your location. Business interruption insurance keeps your business alive while that happens.

For less than 0.5% of your annual revenue, you can protect your income, retain your employees, and ensure you can reopen after disaster strikes.

Get a free business interruption insurance review:

📞 Call: (562) 402-1737

📧 Email: info@pinoygeneralinsurance.com

📍 Visit: 17304 Norwalk Blvd, Cerritos, CA 90703

🌐 Online: pinoygeneralinsurance.com

We'll review your current commercial insurance, calculate your actual business interruption need, and provide quotes from multiple carriers to ensure you're protected properly.

Because your business deserves more than just property coverage—it deserves income protection too.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County businesses protect their property, liability, and income through comprehensive commercial insurance solutions.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.