How to Lower Your Auto Insurance Premium Without Reducing Coverage

You can reduce auto insurance costs by 20-40% without sacrificing protection—here are 15 proven strategies that actually work.

AUTO INSURANCEINSURANCE TIPS

Felix | Pinoy General Insurance Services

2/23/20268 min read

Auto insurance is expensive—and getting more expensive every year. The average California driver now pays $1,800-$2,400/year for full coverage.

But here's what most people don't realize: there are dozens of ways to reduce your premium without lowering your coverage limits or taking on more risk.

At Pinoy General Insurance, we help clients save an average of $600-$900/year on auto insurance by implementing strategies most people never think to ask about.

This guide covers 15 proven methods to lower your auto insurance costs while maintaining the protection you need.

Strategy #1: Shop Your Insurance Every 2-3 Years

Potential savings: 20-35% ($300-$700/year)

Insurance companies adjust their pricing constantly. The carrier that gave you the best rate 3 years ago may no longer be competitive.

Why this works:

Carriers target different demographics at different times

Your risk profile changes (older, more experienced driver = lower rates)

New carriers enter the market with competitive introductory pricing

Action steps:

Get quotes from at least 3-5 carriers

Compare identical coverage (same limits, same deductibles)

Use an independent agent who can shop 10-15 carriers simultaneously

Real example: Cerritos couple paid $2,200/year with Carrier A for 6 years. Shopped competitors, found identical coverage with Carrier B for $1,550/year. Annual savings: $650.

Strategy #2: Bundle Auto + Home Insurance

Potential savings: 15-25% on both policies ($400-$800/year combined)

Most carriers offer significant discounts when you bundle multiple policies.

Why this works:

Lower administrative costs for the carrier

Customer loyalty incentive (you're less likely to switch if you have multiple policies)

Action steps:

Get bundle quotes from carriers that offer both auto and home insurance

Compare bundle savings vs. keeping policies separate

Don't assume bundling is always cheaper—verify the math

Real example:

Auto (Company A): $1,400/year

Home (Company B): $1,600/year

Total: $3,000/year

After bundling with Company C:

Auto: $1,120/year (20% discount)

Home: $1,280/year (20% discount)

New total: $2,400/year

Annual savings: $600

Strategy #3: Increase Your Deductibles Strategically

Potential savings: 15-30% on collision/comprehensive ($200-$450/year)

Your deductible is what you pay out-of-pocket before insurance coverage begins.

Standard deductibles: $500 or $1,000

Savings from increasing deductibles:

$500 → $1,000: Save 15-20%

$500 → $2,000: Save 30-40%

Example:

Current premium with $500 deductible: $1,800/year

New premium with $1,000 deductible: $1,500/year

Annual savings: $300

Additional out-of-pocket risk: $500

When this makes sense:

You have an emergency fund covering the higher deductible

You rarely file claims (if you file a claim every 5+ years, the premium savings outweigh the higher deductible)

When to avoid:

You don't have savings to cover a $1,000-$2,000 deductible

You have a history of frequent small claims

Strategy #4: Remove Unnecessary Coverages

Potential savings: $100-$400/year

Audit your policy for optional coverages you may not need:

Rental Car Reimbursement ($10-$20/month = $120-$240/year)

What it covers: Rental car costs while your vehicle is being repaired after a covered claim.

When to drop it:

You have a second vehicle you can use

You have easy access to rides (family, public transit, rideshare)

You can afford a rental car out-of-pocket if needed

Roadside Assistance ($5-$10/month = $60-$120/year)

What it covers: Towing, jumpstarts, flat tire changes, lockout service.

When to drop it:

You have AAA or another roadside assistance membership

Your car manufacturer provides roadside assistance (many new cars include this)

Collision/Comprehensive on Older Vehicles

Rule of thumb: If your car is worth less than $3,000-$4,000, collision and comprehensive coverage may not be cost-effective.

Example:

Car value: $2,500

Collision + comprehensive premium: $600/year

Deductible: $1,000

If your car is totaled:

Insurance pays: $1,500 ($2,500 value - $1,000 deductible)

You paid: $600 in premium

Break-even: 2.5 years ($600 × 2.5 = $1,500). If you keep the car longer than 2.5 years without a total loss, you've paid more in premiums than you'd receive in a claim.

Better strategy: Drop collision/comprehensive, save $600/year, put that money toward a replacement vehicle fund.

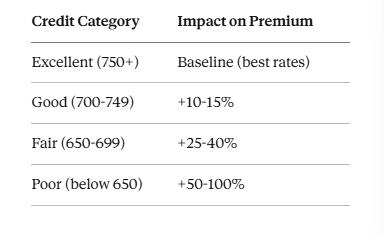

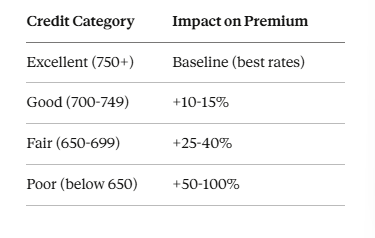

Strategy #5: Improve Your Credit Score

Potential savings: 20-40% ($350-$750/year)

California allows insurers to use credit-based insurance scores when setting rates. Better credit = lower premiums.

Why this works:

Studies show strong correlation between credit scores and claims frequency

Insurers view good credit as a proxy for responsibility

How credit affects auto insurance:

Action steps to improve credit:

Pay all bills on time (35% of your score)

Reduce credit card balances below 30% of limits

Don't close old credit accounts

Dispute errors on your credit report

Timeline: Credit improvements typically take 6-12 months to significantly impact insurance rates. Request a re-quote after major credit improvements.

Strategy #6: Ask About Low Mileage Discounts

Potential savings: 5-15% ($90-$270/year)

Drive less = lower accident risk = lower premium.

Qualification:

Typically under 7,500-10,000 miles/year

Some carriers offer tiered discounts (under 5,000 miles = bigger discount)

Why many people miss this:

They reported higher mileage when they bought the policy (commuting to work)

Life changed (now working from home) but they never updated their policy

Action steps:

Review your current policy—what annual mileage did you report?

Check your actual annual mileage (odometer reading ÷ years owned)

If you're driving significantly less, call your carrier and request a mileage update

Real example: Client reported 15,000 miles/year on her policy. Started working from home in 2020, now drives 6,000 miles/year. Updated mileage with carrier, saved $180/year.

Strategy #7: Enroll in Usage-Based (Telematics) Insurance

Potential savings: 10-40% ($180-$720/year)

Apps or plug-in devices monitor your driving and reward safe habits.

Programs available:

Progressive Snapshot

State Farm Drive Safe & Save

Allstate Drivewise

Nationwide SmartRide

What they monitor:

Miles driven

Hard braking events

Speeding

Time of day (late-night driving increases risk)

Who saves the most:

Low-mileage drivers

Drivers who avoid hard braking

Drivers who stay within speed limits

Drivers who avoid late-night driving (11pm-4am)

Privacy concerns? These programs are voluntary. If you're uncomfortable with tracking, skip this discount. But for safe, low-mileage drivers, it's one of the biggest savings opportunities.

Strategy #8: Take a Defensive Driving Course

Potential savings: 5-15% ($90-$270/year)

Completing an approved defensive driving course can reduce premiums for 3 years.

Requirements:

Course must be approved by your insurance carrier

Typically 4-8 hours (online or in-person)

Cost: $20-$50

Return on investment:

Premium savings: $150/year × 3 years = $450

Course cost: $30

Net savings: $420 over 3 years

Who saves the most:

Drivers 55+ (often receive larger discounts)

Drivers under 25 (can offset young driver surcharges)

Action steps:

Ask your carrier for a list of approved courses

Complete the course

Submit your certificate to your carrier

Strategy #9: Remove Drivers Who No Longer Live With You

Potential savings: $500-$2,000/year (depending on driver's age/history)

If a listed driver moves out (adult child goes to college, ex-spouse after divorce), remove them from your policy immediately.

Common scenarios:

Teen driver goes to college 100+ miles away without a car

Adult child moves out and gets their own insurance

Divorce/separation

Important: Only remove drivers who truly no longer live with you or have access to your vehicles. Failing to list household members who drive is insurance fraud.

College student exception: If your child is away at school 100+ miles from home without a car, many carriers offer a "student away at school" discount that reduces (but doesn't eliminate) their premium impact.

Strategy #10: Anti-Theft Device Discount

Potential savings: 5-15% on comprehensive coverage ($50-$150/year)

Vehicles with anti-theft devices are less likely to be stolen.

Qualifying devices:

Factory-installed alarms and immobilizers

GPS tracking systems (LoJack, OnStar)

Steering wheel locks (The Club)

VIN etching

Why people miss this:

Modern vehicles (2015+) have factory alarms/immobilizers, but owners never notify their carrier

Aftermarket systems are installed but never reported to insurance

Action steps:

Check if your vehicle has a factory alarm or immobilizer (most 2015+ vehicles do)

Notify your carrier and request the discount

If you install an aftermarket system, submit proof to your carrier

Strategy #11: Good Student Discount (For Teen Drivers)

Potential savings: 10-25% ($300-$800/year on the teen driver's portion)

Teen drivers with B averages or higher qualify for significant discounts.

Requirements:

Typically 3.0 GPA or higher

Full-time student (high school or college)

Under age 25

Why this matters:

Adding a teen driver increases premiums by 50-100%

Good student discount offsets 10-25% of that increase

Example:

Premium before teen driver: $1,200/year

After adding teen (no discount): $2,400/year (+$1,200)

After adding teen with 20% good student discount: $2,160/year (+$960)

Savings: $240/year

Action steps:

Request a copy of your teen's report card or transcript

Submit to your carrier

Resubmit annually to maintain the discount

Strategy #12: Professional Association & Affinity Group Discounts

Potential savings: 5-15% ($90-$270/year)

Many carriers offer discounts for members of specific organizations:

Common qualifying groups:

AAA (auto club membership)

AARP (age 50+)

Alumni associations

Professional organizations (engineers, teachers, nurses, military)

Employer groups (some large employers have group insurance agreements)

Action steps:

Review your memberships—are you part of any professional or affinity groups?

Ask your carrier which organizations qualify for discounts

Provide proof of membership

Real example: Client belonged to her college alumni association (membership: $50/year). Carrier offered 8% alumni discount, saving $160/year. Net savings after membership cost: $110/year.

Strategy #13: Pay Annually Instead of Monthly

Potential savings: 5-10% ($90-$240/year)

Paying your full annual premium in one payment eliminates monthly installment fees.

Why monthly payments cost more:

Installment fees: Typically $3-$10/month

Some carriers charge interest on monthly payment plans

Example:

Annual premium: $1,200

Monthly payment: $105/month × 12 = $1,260

Difference: $60/year (5%)

Strategy if you can't afford annual payment now:

Save your monthly premium amount in a high-yield savings account

After 12 months, you'll have saved enough to pay the next year's premium in full

Strategy #14: Review and Optimize Your Liability Limits

Savings potential: Varies (but don't sacrifice protection for savings)

This is nuanced—you want adequate liability coverage, but you also don't want to overpay.

If you have LOW liability limits ($15,000/$30,000):

Don't reduce them further—you're already dangerously underinsured

Increase to $100,000/$300,000—yes, this costs more, but it protects you from financial ruin

If you have VERY HIGH liability limits ($500,000/$1,000,000) but don't need them:

Consider whether umbrella insurance would be more cost-effective

$100,000/$300,000 auto liability + $1 million umbrella often costs less than $1 million auto liability alone

Action steps:

Review your current liability limits

Calculate your net worth (assets worth protecting)

Ensure liability + umbrella = adequate protection without overpaying

Strategy #15: Drop Duplicate Coverages

Potential savings: $50-$200/year

Some coverages may duplicate protection you already have elsewhere:

Medical Payments Coverage

What it covers: Medical bills for you and passengers after an accident, regardless of fault.

When to consider dropping:

You have comprehensive health insurance with low deductibles/copays

You're duplicating coverage

When to keep:

Your health insurance has high deductibles ($5,000+)

You frequently have passengers who may not have health insurance

Towing and Labor Coverage

What it covers: Towing costs, roadside assistance.

When to consider dropping:

You have AAA or another roadside service

Your car manufacturer provides roadside assistance

Strategies to AVOID (Don't Sacrifice Protection for Savings)

❌ Reducing liability limits below $100,000/$300,000

Saving $200/year isn't worth the risk of personal financial ruin from a lawsuit.

❌ Dropping uninsured/underinsured motorist coverage

15%+ of California drivers are uninsured. This coverage protects you when they hit you.

❌ Canceling your policy to avoid payments

Gaps in coverage increase future premiums significantly. If you can't afford your current policy, find a cheaper one before canceling.

❌ Lying about mileage, garaging location, or drivers

Insurance fraud can result in denied claims and policy cancellation.

How to Implement These Strategies

Step 1: Audit Your Current Policy

Pull out your declarations page and identify:

Current coverage limits

Current deductibles

Discounts currently applied

Optional coverages you're paying for

Step 2: Prioritize High-Impact Changes

Focus on strategies with the biggest savings:

Shop multiple carriers (20-35% savings)

Bundle policies (15-25% savings)

Increase deductibles (15-30% savings on collision/comp)

Improve credit score (20-40% savings)

Usage-based insurance (10-40% savings)

Step 3: Make the Changes

Contact your current carrier or work with an independent agent to implement changes.

Step 4: Review Annually

Set a calendar reminder to review your policy every year:

Shop competitors

Update mileage, drivers, vehicles

Look for new discounts

How Pinoy General Insurance Can Help

We specialize in finding every available discount and comparing carriers to get you the lowest price for the coverage you need.

What we do: ✅ Shop 15+ carriers simultaneously

✅ Identify all discounts you qualify for

✅ Optimize coverage to eliminate waste without sacrificing protection

✅ Review your policy annually for new savings opportunities

Free auto insurance review:

📞 Call: (562) 402-1737

📧 Email: info@pinoygeneralinsurance.com

📍 Visit: 17304 Norwalk Blvd, Cerritos, CA 90703

🌐 Online: pinoygeneralinsurance.com

We'll review your current policy, implement these savings strategies, and show you exactly how much you can save.

Final Thoughts

You don't have to sacrifice coverage to lower your auto insurance costs. Strategic changes—shopping carriers, bundling policies, improving credit, claiming discounts—can reduce your premium by 20-40% while maintaining the same protection.

The average family implementing just 5 of these strategies saves $600-$900/year.

That's $600-$900 you could put toward savings, debt, or anything else that matters more than overpaying for insurance.

Take 30 minutes this week to implement these strategies. Your bank account will thank you.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Southern California drivers save money on auto insurance while maintaining comprehensive protection.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.