Insurance for Rideshare Drivers: What Uber and Lyft Drivers in Cerritos Must Know

Personal auto insurance doesn't cover rideshare driving—here's what coverage you actually need and how to avoid devastating coverage gaps.

AUTO INSURANCEINSURANCE TIPS

Felix | Pinoy General Insurance Services

3/2/20266 min read

If you drive for Uber or Lyft using only your personal auto insurance, you're driving uninsured for significant portions of every shift.

Most rideshare drivers don't realize this until they're in an accident and their insurance company denies the claim because they were "driving for commercial purposes."

Rideshare insurance is complicated because coverage changes depending on which "period" you're in:

Period 0: App is off (personal insurance covers you)

Period 1: App is on, waiting for ride request (coverage gap)

Period 2: Ride accepted, driving to pick up passenger (limited Uber/Lyft coverage)

Period 3: Passenger in car (full Uber/Lyft coverage)

Understanding these periods and how to fill coverage gaps is critical for every rideshare driver in California.

The Coverage Gap That Costs Rideshare Drivers Thousands

What Uber and Lyft Provide

Period 1 (App on, no ride request):

Liability: $50,000 per person / $100,000 per accident / $25,000 property damage

No collision or comprehensive coverage (if you damage your own car, you pay 100%)

Period 2 (Ride accepted, driving to pickup):

Liability: $1 million

Uninsured/underinsured motorist: $1 million

Collision: $2,500 deductible (if you have collision on personal policy)

Comprehensive: $2,500 deductible (if you have comprehensive on personal policy)

Period 3 (Passenger in car):

Liability: $1 million

Uninsured/underinsured motorist: $1 million

Collision: $2,500 deductible

Comprehensive: $2,500 deductible

The Problem: Period 1 Coverage Gaps

When you turn on the app but haven't accepted a ride yet, you have:

✅ Liability coverage (but only $50K/$100K—barely more than California minimum)

❌ NO collision coverage (damage to your car)

❌ NO comprehensive coverage (theft, vandalism, weather damage)

Real scenario: Cerritos Uber driver has app on, waiting for ride request. Gets rear-ended at a red light. The at-fault driver has minimum insurance ($15,000). Uber driver's car has $8,000 in damage.

What happens:

At-fault driver's insurance pays: $8,000 (fortunately, enough to cover damage)

Uber's Period 1 coverage: Not needed this time

Driver's personal insurance: Won't pay (driver was logged into rideshare app)

Now imagine the driver was at fault:

At-fault driver's insurance: $0 (driver was at fault)

Uber's Period 1 collision coverage: $0 (Uber doesn't provide collision in Period 1)

Driver's personal collision coverage: DENIED (commercial use exclusion)

Driver pays $8,000 out-of-pocket

This is the coverage gap that destroys rideshare drivers financially.

What You Need: Rideshare Insurance Coverage

Option 1: Rideshare Endorsement (Add-On to Personal Policy)

What it is: An endorsement added to your personal auto policy that fills Period 1 coverage gaps.

What it covers:

Collision and comprehensive during Period 1 (app on, no ride)

Often includes lower deductibles than Uber/Lyft's $2,500

Cost: $10-$30/month additional

Available from:

Mercury

Progressive

Nationwide

Pros:

Fills the Period 1 gap

Often cheaper than commercial policy

Keeps your personal insurance intact

Cons:

Not all carriers offer this

May have limitations on hours driven

This is the best option for most part-time rideshare drivers.

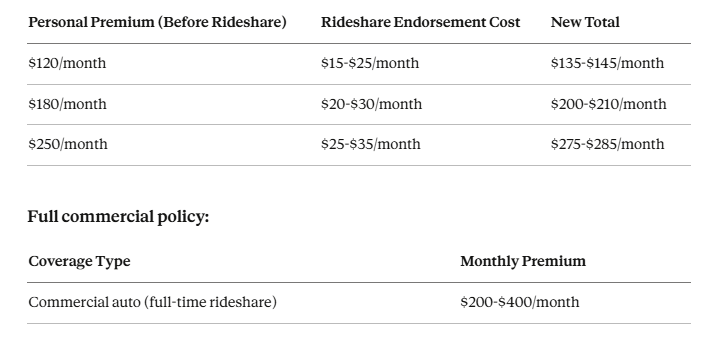

Option 2: Commercial Auto Insurance

What it is: Full commercial coverage designed for rideshare and delivery drivers.

Cost: $200-$400/month (significantly more expensive than rideshare endorsement)

Who needs this:

Full-time rideshare drivers (40+ hours/week)

Drivers who also do food/package delivery

Drivers whose personal carrier doesn't offer rideshare endorsements

Pros:

Comprehensive coverage for all periods

No coverage gaps

Designed specifically for commercial driving

Cons:

Very expensive

May not be cost-effective for part-time drivers

Option 3: Hybrid Approach

What it is: Personal policy with rideshare endorsement + understanding Uber/Lyft's coverage

What you have:

Period 0 (app off): Personal insurance

Period 1 (app on, no ride): Personal insurance + rideshare endorsement

Periods 2-3 (ride accepted/passenger in car): Uber/Lyft insurance + your collision/comprehensive (with $2,500 deductible)

This is what most Cerritos rideshare drivers should have.

What Happens If You Don't Tell Your Insurance Company You Drive Rideshare?

Scenario: You drive for Uber but never told your insurance company. You get in an accident while the app is on.

Possible outcomes:

Best case (very rare):

Your insurance company doesn't find out you were driving rideshare

They pay your claim

You got lucky (but you committed insurance fraud)

Likely case:

Insurance company investigates

Discovers you were logged into Uber app

Denies your claim

You pay for all damages out-of-pocket

Worst case:

Insurance company denies claim

Cancels your policy for material misrepresentation (fraud)

Reports you to other carriers

You're now in the high-risk pool, paying 2-3x normal premiums for years

You may face legal consequences for insurance fraud

Don't hide rideshare driving from your insurer. It's not worth the risk.

How Much Does Rideshare Insurance Cost in California?

Adding rideshare endorsement to existing personal policy:

Factors that affect cost:

How many hours/week you drive

Your driving record

Vehicle type and value

Coverage limits and deductibles

Location (urban areas cost more)

Step-by-Step: How to Get Proper Rideshare Coverage

Step 1: Contact Your Current Auto Insurance Carrier

Call your current insurer and say:

"I drive for Uber/Lyft part-time. I need to add rideshare coverage to my policy. Do you offer a rideshare endorsement?"

If yes:

Get a quote for the endorsement

Understand what it covers (Period 1 gaps, right?)

Add it to your policy immediately

If no:

Ask if they'll still cover you with rideshare driving disclosed

Many carriers will decline to insure rideshare drivers at all

Step 2: Shop Rideshare-Friendly Carriers (If Needed)

If your current carrier doesn't offer rideshare coverage:

Carriers that offer rideshare endorsements:

Allstate (Ride for Hire)

State Farm

Farmers

Progressive

Nationwide

GEICO (varies by state)

Get quotes from at least 3 carriers with rideshare endorsements.

Step 3: Compare Total Cost

Calculate:

Personal premium + rideshare endorsement

vs. Commercial policy cost

vs. Risk of driving uninsured in Period 1

For most part-time drivers: Personal + rideshare endorsement is the most cost-effective option.

Step 4: Purchase and Update Your Rideshare App

Once you have proper coverage:

Upload your new insurance card to Uber/Lyft

Keep proof of rideshare coverage in your vehicle

Notify Uber/Lyft immediately if your policy changes

Understanding the Four Periods of Rideshare Coverage

Period 0: App Off (Personal Insurance Applies)

You're covered by: Your personal auto insurance

What's covered:

Liability

Collision (if you have it)

Comprehensive (if you have it)

No issues here—you're driving for personal use.

Period 1: App On, Waiting for Ride (THE GAP)

You're covered by:

Uber/Lyft: $50K/$100K liability only

Your personal insurance: Maybe (only if you have rideshare endorsement)

What's NOT covered by Uber/Lyft:

❌ Collision (damage to your car if you're at fault)

❌ Comprehensive (theft, vandalism, weather damage)

Without rideshare endorsement:

You're driving uninsured for collision/comprehensive

If you damage your car, you pay 100% out-of-pocket

With rideshare endorsement:

Your personal policy fills the gap

You have full collision/comprehensive coverage

Period 2: Ride Accepted, Driving to Pickup

You're covered by: Uber/Lyft (primary) + your personal policy (excess)

Uber/Lyft provides:

$1 million liability

$1 million uninsured/underinsured motorist

Collision with $2,500 deductible

Comprehensive with $2,500 deductible

Much better coverage, but that $2,500 deductible is high.

Period 3: Passenger in Car

You're covered by: Uber/Lyft (same as Period 2)

Full $1 million coverage for liability and uninsured motorist.

Collision/comprehensive with $2,500 deductible.

Common Rideshare Insurance Mistakes

Mistake #1: Not Disclosing Rideshare Driving

Why it's a problem: Insurance fraud, denied claims, policy cancellation.

Fix: Disclose rideshare driving to your insurer and add proper coverage.

Mistake #2: Assuming Uber/Lyft Coverage Is Enough

Why it's a problem: Period 1 has no collision/comprehensive. You're exposed during wait times.

Fix: Add rideshare endorsement to cover Period 1 gaps.

Mistake #3: Driving Without Checking Coverage Periods

Why it's a problem: You might think you're covered when you're not.

Fix: Understand exactly what's covered in each period and plan accordingly.

Mistake #4: Keeping Collision on an Old Car

Why it's a problem: If your car is worth $3,000 but you're paying $600/year for collision with a $1,000 deductible, you're wasting money.

Fix: Drop collision/comprehensive on older vehicles, save premiums.

Mistake #5: Not Shopping for Better Rates

Why it's a problem: Rideshare-friendly carriers vary significantly in pricing.

Fix: Get quotes from multiple carriers annually.

Tax Deductions for Rideshare Insurance

Good news: Rideshare insurance premiums are tax-deductible business expenses.

What you can deduct:

The portion of your premium attributable to rideshare driving

If you drive rideshare 30% of the time, you can deduct approximately 30% of your premium

Keep records:

Mileage logs (rideshare miles vs. personal miles)

Insurance premium statements

Receipts for all vehicle-related expenses

Consult a tax professional for specific guidance on deductions.

What to Do After an Accident While Rideshare Driving

Step 1: Ensure Safety

Check for injuries

Call 911 if anyone is hurt

Move to a safe location if possible

Step 2: Document Everything

Take photos of all vehicles and damage

Get other driver's insurance information

Get witness contact information

Note which period you were in (app on/off, passenger in car, etc.)

Step 3: Report to Appropriate Parties

If you were in Period 0 (app off):

Report to your personal insurance only

If you were in Period 1, 2, or 3 (app on):

Report to Uber/Lyft immediately through the app

Report to your personal insurance (especially if you have rideshare endorsement)

Step 4: Follow Up

Work with Uber/Lyft's insurance team

Coordinate with your personal insurance if needed

Keep all documentation organized

Final Thoughts

Rideshare driving without proper insurance is a financial time bomb. The coverage gaps are real, and thousands of drivers learn this the hard way every year.

The cost of a rideshare endorsement ($15-$30/month) is minimal compared to the risk of being uninsured during Period 1.

Don't wait until after an accident to fix your coverage. Do it today.

Need help with rideshare insurance?

📞 Call: (562) 402-1737

📧 Email: info@pinoygeneralinsurance.com

📍 Visit: 17304 Norwalk Blvd, Cerritos, CA 90703

🌐 Online: pinoygeneralinsurance.com

We work with multiple carriers that offer rideshare endorsements. We'll help you:

Determine exactly what coverage you need

Compare quotes from rideshare-friendly carriers

Add proper coverage at the best price

Stay compliant with Uber/Lyft requirements

Because one denied claim can cost more than a lifetime of proper coverage.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Southern California drivers—including rideshare and delivery drivers—secure proper coverage.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.