Key Person Insurance: Protecting Your Business from the Loss of Critical Employees

How key person life insurance protects businesses from financial devastation when critical employees die or become disabled.

BUSINESS INSURANCESPECIALTY INSURANCE

Felix | Pinoy General Insurance Services

3/23/202612 min read

Your top salesperson generates 40% of your company's revenue. She dies unexpectedly in a car accident.

Within three months:

Revenue drops by $500,000

You scramble to hire and train a replacement (cost: $80,000)

Clients leave because of the disruption

Your bank threatens to call your business loan

You're forced to take a salary cut to keep the business afloat

One year later, your business is still struggling to recover. You've lost $800,000 in revenue, spent $150,000 on recruitment and training, and accumulated $200,000 in additional debt.

Total financial impact: Over $1 million.

A $1 million key person life insurance policy would have cost you $2,500/year. Instead, you're facing potential bankruptcy.

This scenario plays out in small businesses across California every year. Most business owners never consider what would happen if their most critical employee—or they themselves—suddenly died or became disabled.

After helping Orange County businesses protect themselves since 1993, I can tell you exactly what key person insurance is, who needs it, how much coverage to buy, and how it can save your business from financial catastrophe.

What Is Key Person Insurance?

Simple Definition: Life insurance owned by a business on the life of a critical employee, with the business as the beneficiary.

How It Works:

Business identifies "key person" - employee whose death would cause significant financial harm

Business purchases life insurance policy on that person's life

Business pays premiums (usually tax-deductible as business expense)

Business is the owner and beneficiary of the policy

If key person dies, business receives death benefit tax-free

Business uses proceeds to:

Replace lost revenue

Recruit and train replacement

Pay off debts

Reassure lenders/investors

Keep business operating during transition

This is NOT the same as:

Personal life insurance (owned by individual, benefits family)

Group life insurance (benefits employees' families)

Buy-sell insurance (funds buyout of deceased owner's shares)

Key person insurance protects the BUSINESS from financial loss when a critical employee dies.

Who Qualifies as a "Key Person"?

A key person is anyone whose death or disability would cause significant financial harm to your business.

Common Examples:

1. Business Owner/Founder

Especially in businesses dependent on owner's expertise, relationships, or reputation

Loss would devastate operations and revenue

Often the most obvious key person

2. Top Sales Producer

Generates significant portion of revenue

Has established client relationships

Would take months or years to replace revenue stream

Example: Sales rep generates $2 million in annual revenue with 20% profit margin = $400,000 in annual profit lost if they die.

3. Specialized Technical Expert

Possesses rare skills or knowledge

Critical to product development or service delivery

Difficult or impossible to replace quickly

Example: Software engineer who built your proprietary system and is the only one who fully understands it.

4. Key Manager/Executive

Manages critical operations

Maintains key vendor/client relationships

Departure would disrupt business operations

5. Creative Talent

Designer, architect, chef, artist whose work defines your brand

Loss would damage brand reputation and client relationships

6. Licensed Professional

Doctor, lawyer, architect, engineer whose license allows business to operate

Loss could prevent business from legally operating in certain areas

Questions to Identify Key Persons:

Ask yourself:

Whose death would immediately impact revenue by 20%+ ?

Who would be extremely difficult to replace within 6-12 months?

Who has relationships with your most important clients?

Who possesses unique knowledge or skills critical to operations?

Whose loss would cause your bank to demand loan repayment?

Who would your competitors try to hire away (if they could)?

If you answer "yes" to 2+ questions for any employee, they're likely a key person.

Real Example - Cerritos Manufacturing Company:

15-employee precision manufacturing business

Key Persons Identified:

Owner (age 58): Client relationships, industry expertise, provides financing guarantee

Lead Engineer (age 52): Only person who understands proprietary manufacturing process

Top Salesperson (age 45): Generates 60% of revenue through long-term client relationships

Risk Assessment:

Owner's death: Bank calls $500K loan, clients leave, business likely closes

Engineer's death: Cannot fulfill existing contracts, $300K+ in lost revenue

Salesperson's death: Lose $1.2M in annual revenue, takes 2+ years to rebuild

Solution:

$1M policy on owner

$500K policy on engineer

$1M policy on salesperson

Total annual premium: $6,200

Total protection: $2.5M

Cost of being uninsured: Potential business closure worth $3-5M.

How Much Key Person Insurance Do You Need?

There's no single formula, but here are three approaches:

Method 1: Multiple of Salary

Simple approach: 5-10x the key person's annual salary

Example:

Key employee salary: $120,000

Coverage: $600,000-$1,200,000

Pros: Easy to calculate Cons: Doesn't account for actual revenue impact or replacement costs

Method 2: Revenue Impact Analysis

More accurate approach: Calculate revenue/profit attributable to key person, multiply by years to replace.

Formula: (Annual revenue generated × Profit margin) × Years to replace

Example - Top Salesperson:

Annual sales generated: $2,000,000

Profit margin: 25%

Annual profit contribution: $500,000

Time to replace and rebuild: 2-3 years

Coverage needed: $1,000,000-$1,500,000

Example - Technical Expert:

Annual revenue dependent on their expertise: $800,000

Profit margin: 30%

Annual profit contribution: $240,000

Time to find/train replacement: 2 years

Additional costs: Recruiting ($50K), training ($30K), interim consulting ($100K)

Coverage needed: $660,000-$750,000

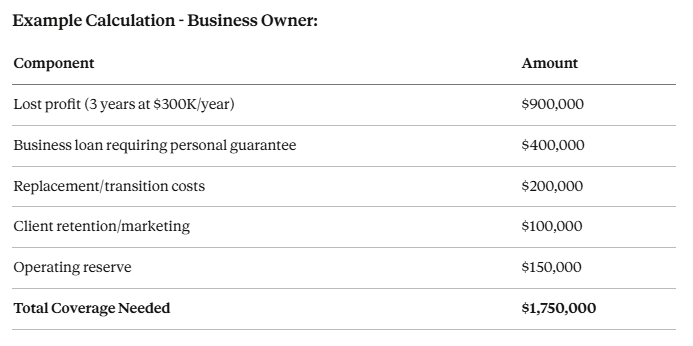

Method 3: Comprehensive Financial Impact

Most thorough approach: Calculate total financial impact of loss.

Components to Include:

Lost Revenue/Profit

Annual profit contribution × years to recover

Replacement Costs

Recruiting fees: $50,000-$150,000 (20-30% of salary)

Signing bonus/relocation: $20,000-$100,000

Training costs: $30,000-$80,000

Reduced productivity during ramp-up: $50,000-$200,000

Debt Coverage

Outstanding business loans that might be called

Line of credit that might be pulled

SBA loans requiring key person guarantee

Opportunity Costs

Lost contracts/bids during disruption

Damaged client relationships

Competitive disadvantage

Stabilization Reserve

Operating capital during transition

Marketing to reassure clients

Retention bonuses for remaining staff

Round to: $1,500,000 or $2,000,000 policy

General Guidelines:

Business Owner: $500,000-$5,000,000 (depending on business size/revenue)

Top Sales Producer: $500,000-$2,000,000

Key Executive: $250,000-$1,500,000

Technical Expert: $250,000-$1,000,000

Specialized Professional: $300,000-$1,000,000

Multiple Key Persons:

If you have 2-3 key persons, you need separate policies on each, OR one large policy that can be split among multiple losses.

Types of Key Person Insurance: Term vs. Permanent

You have two main options:

Term Life Insurance

How it works:

Coverage for specific period (10, 20, 30 years)

Level premiums during term

No cash value

Coverage expires at end of term

Best for:

Temporary key person situations

Budget-conscious businesses

Younger key employees (long coverage period needed)

When you only need coverage while person is employed

Pros:

Much lower premiums (50-70% cheaper than permanent)

Straightforward coverage

Easy to understand

Flexibility to adjust coverage as needed

Cons:

No cash value buildup

Coverage ends (must renew at higher rates)

Premiums increase at renewal

No permanent protection

Cost Example:

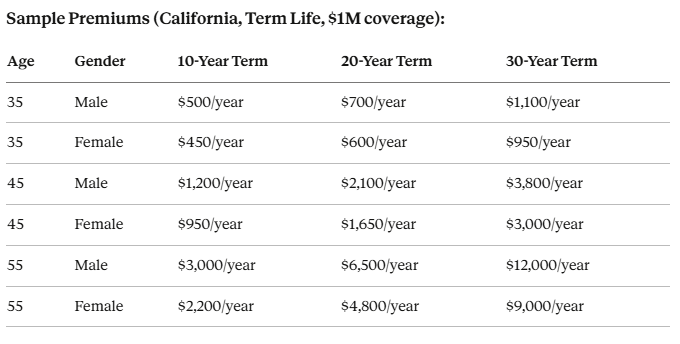

$1M term policy, 45-year-old non-smoker: $1,200-$1,800/year

Permanent Life Insurance (Whole Life, Universal Life)

How it works:

Coverage for entire lifetime

Premiums build cash value

Can borrow against cash value

Premiums guaranteed or flexible (depending on type)

Best for:

Long-term key person (owner, partner)

Business wanting to build asset on balance sheet

When you want to retain policy after key person leaves

Executive compensation/retention strategy

Pros:

Coverage never expires

Builds cash value (business asset)

Can borrow against cash value for business needs

Can be used as executive benefit/golden handcuff

Cons:

Much higher premiums (2-4x more than term)

More complex

Takes years to build significant cash value

Lower death benefit per dollar of premium

Cost Example:

$1M whole life policy, 45-year-old non-smoker: $8,000-$12,000/year

Which Should You Choose?

Choose Term Life if: ✅ Budget is tight ✅ Need maximum coverage per premium dollar ✅ Key person is not owner (will eventually leave/retire) ✅ Business is young/growing (maximize protection now) ✅ Want simplicity

Choose Permanent Life if: ✅ Key person is owner (permanent need) ✅ Want to build business asset (cash value) ✅ Plan to use as executive compensation ✅ Can afford higher premiums ✅ Want to retain policy after key person transitions out

Hybrid Approach:

Many businesses use BOTH:

Large term policy for maximum protection (e.g., $2M term)

Smaller permanent policy for cash value/long-term coverage (e.g., $500K whole life)

Total coverage: $2.5M with balanced cost

Tax Implications of Key Person Insurance

Understanding the tax treatment is critical:

Premiums:

General Rule: Premiums paid by business are NOT tax-deductible.

Why: IRS considers this personal insurance benefit, not ordinary business expense.

Exception: In rare cases with special structuring, partial deductibility may be available. Consult tax professional.

Death Benefit:

Good News: Death benefit received by business is generally TAX-FREE under IRC Section 101(a).

Requirements for tax-free treatment:

Business is owner and beneficiary

Insured was employee at time of policy issuance

Business notified insured of coverage

Policy was not transferred-for-value

Example:

Business receives $1,000,000 death benefit

Pays $0 federal income tax on proceeds

Can use full $1,000,000 for business recovery

Cash Value:

If permanent policy with cash value:

Cash value grows tax-deferred

Business can borrow against cash value tax-free

Must repay loans with interest or death benefit is reduced

Alternative Minimum Tax (AMT):

Corporate AMT was eliminated in 2018, so death benefits are now fully tax-free for corporations without AMT implications.

Important: Tax laws change. Consult CPA or tax attorney for current rules and your specific situation.

How to Buy Key Person Insurance

Step 1: Identify Key Persons

Use the criteria discussed earlier. List:

Name and role

Why they're critical

Estimated financial impact of loss

Step 2: Calculate Coverage Amounts

Use one of the three methods:

Multiple of salary (quick estimate)

Revenue impact analysis (more accurate)

Comprehensive financial impact (most thorough)

Step 3: Choose Policy Type

Decide between:

Term (lower cost, temporary coverage)

Permanent (higher cost, cash value, lifetime coverage)

Hybrid (both)

Step 4: Get Quotes

Work with:

Independent insurance agent (can quote multiple companies)

Business insurance specialist

Agent familiar with key person insurance

You'll need:

Key person's age, health history, occupation

Desired coverage amount

Preferred policy type and term length

Business information (type, revenue, years established)

Step 5: Medical Underwriting

For policies over $250,000-$500,000:

Key person must complete health questionnaire

May require medical exam (blood test, vitals, urine sample)

Medical records may be requested

Exam is free, usually done at workplace or home

For smaller policies:

Simplified underwriting (health questions only)

No medical exam

Faster approval

Important: Key person must consent to being insured and complete medical underwriting.

Step 6: Business Resolution

Business should pass formal resolution stating:

Why insurance is needed

Amount of coverage

Authorization to purchase

Who has authority to make changes

Maintains documentation that policy serves legitimate business purpose.

Step 7: Set Up Policy

Business applies as owner and beneficiary

Key person completes medical underwriting

Business pays first premium

Policy issued

Typical timeline: 4-8 weeks from application to policy issuance.

Step 8: Maintain Policy

Pay premiums on time (usually annual or quarterly)

Review coverage annually (is amount still adequate?)

Update beneficiary if business structure changes

Notify insurer of key person employment status changes

What Happens When You Receive a Death Benefit

If your key person dies, here's the process:

Step 1: File Claim (Immediately)

Contact insurance company:

Provide death certificate

Complete claim forms

Provide policy information

Step 2: Claim Processing

Timeline:

Simple claims: 2-4 weeks

Complex claims (investigation needed): 1-3 months

Documentation required:

Certified death certificate

Completed claim forms

Beneficiary verification

Policy documents

Step 3: Receive Proceeds

Payment typically by:

Check to business

Wire transfer to business account

Held in interest-bearing account

Amount: Full death benefit, tax-free

Step 4: Use Proceeds Strategically

Recommended uses:

Replace Lost Revenue (primary purpose)

Cover operating expenses during transition

Maintain cash flow

Recruit and Train Replacement

Recruiting fees

Signing bonuses

Training costs

Interim consulting/contractors

Reassure Stakeholders

Demonstrate financial stability to bank

Show clients business will continue

Retain remaining key employees

Pay Down Debt (if appropriate)

Satisfy loan covenants

Reduce financial obligations

Free up cash flow

Operating Reserve

Build cash cushion for transition period

Handle unexpected issues

Buy time to stabilize

What NOT to do: ❌ Distribute as bonuses (defeats purpose) ❌ Use for non-essential expenses ❌ Expand/acquire before stabilizing (too risky)

Key Person Insurance vs. Buy-Sell Insurance

These are often confused but serve different purposes:

Key Person Insurance:

Purpose: Protect business from financial loss when key employee dies

Owner: Business

Beneficiary: Business

Proceeds used for: Revenue replacement, recruitment, debt payment, operations

Who's insured: Any key employee (owner or non-owner)

Buy-Sell Insurance:

Purpose: Fund buyout of deceased owner's business interest

Owner: Individual owners or business (depending on structure)

Beneficiary: Surviving owners or business

Proceeds used for: Purchasing deceased owner's shares/interest

Who's insured: Business owners/partners only

You may need BOTH:

Example - Two-Partner Business:

Partner A and Partner B each own 50%:

Buy-Sell Insurance:

$1M policy on Partner A (owned by Partner B)

$1M policy on Partner B (owned by Partner A)

Purpose: Fund buyout of deceased partner's 50% interest

Key Person Insurance:

$500K policy on Partner A (owned by business)

$500K policy on Partner B (owned by business)

Purpose: Replace lost revenue/expertise during transition

Total coverage: $1.5M on each partner, serving two distinct purposes.

Real-World Key Person Insurance Scenarios

Scenario 1: Orange County Restaurant - Chef Dies

Successful restaurant built around celebrity chef's reputation

Situation:

Chef (age 52) dies of heart attack

Restaurant known for chef's unique creations

Revenue: $2M/year, profit: $400K

Without Key Person Insurance:

Customers stop coming (chef was the draw)

Revenue drops 70% within 3 months

Cannot find replacement chef with same reputation

Forced to close after 8 months

Owner loses $2M investment

With $1M Key Person Insurance:

Uses proceeds to:

Hire two experienced chefs ($300K recruiting/signing bonus)

Rebrand restaurant ($150K marketing)

Cover 6 months operating losses ($200K)

Operating reserve ($350K)

Business survives transition

Rebuilds to 80% of previous revenue within 18 months

Scenario 2: Cerritos Tech Company - Lead Developer Dies

Software company with proprietary platform

Situation:

Lead developer (age 38) dies in accident

Only person who fully understands codebase

Annual revenue: $1.5M, heavily dependent on platform

Without Key Person Insurance:

Cannot maintain or update platform

Existing clients experience bugs/issues

New development grinds to halt

Clients leave for competitors

Company value plummets

Forced to sell assets for $200K (was worth $3M)

With $750K Key Person Insurance:

Hires two senior developers ($200K recruiting)

Brings in specialized consultant ($150K) to document codebase

Covers reduced revenue during 12-month transition ($300K)

Retains remaining technical team with bonuses ($100K)

Successfully transitions, maintains most clients

Business worth $2.5M within 2 years

Scenario 3: Professional Services Firm - Founding Partner Dies

Law firm with three partners

Situation:

Founding partner (age 62) dies

Manages largest clients ($800K/year in billings)

Personal guarantee on $600K line of credit

Without Key Person Insurance:

Bank calls line of credit ($600K due immediately)

Clients uncertain about continuity

40% of clients leave within 6 months

Remaining partners must cover deceased partner's buyout AND lost revenue

Firm nearly bankrupts, eventually sells practice at discount

With $1.5M Key Person Insurance:

Pays off line of credit ($600K) - bank satisfied

Funds deceased partner's buyout per buy-sell agreement ($500K)

Transition costs and client retention ($200K)

Operating reserve ($200K)

Firm remains stable, retains 80% of clients

Successfully transitions over 18 months

Common Thread: Key person insurance provided financial stability during crisis, allowing business to survive and recover.

Common Mistakes to Avoid

Mistake #1: Waiting Too Long

"We'll get key person insurance next year when we're more profitable."

Problem: Key person could die/become disabled before you buy coverage.

Solution: Buy coverage as soon as you identify key persons. Term insurance is affordable even for small businesses.

Mistake #2: Inadequate Coverage

Buying $250K policy when you need $1M to avoid higher premiums.

Problem: Partial coverage doesn't prevent business failure.

Solution: Calculate actual financial impact. Buy adequate coverage even if premiums are higher.

Mistake #3: Only Insuring the Owner

"I'm the only key person in my business."

Reality: Your top salesperson, lead engineer, or key manager may be just as critical.

Solution: Objectively assess all key persons, not just ownership.

Mistake #4: Wrong Policy Type

Buying permanent insurance when term would be better (or vice versa).

Problem: Either overpaying for unnecessary features or lacking features you need.

Solution: Match policy type to your situation and budget.

Mistake #5: Not Reviewing Coverage Regularly

Bought policy 10 years ago, never reviewed.

Problem: Business has grown, original coverage now inadequate.

Solution: Review annually. Increase coverage as business value grows.

Mistake #6: Poor Documentation

No business resolution, unclear purpose for policy.

Problem: IRS could challenge tax-free status of death benefit.

Solution: Proper documentation showing legitimate business purpose.

Mistake #7: Not Telling Key Person

Buying insurance on employee without their knowledge.

Problem: Requires key person consent and participation in underwriting.

Solution: Discuss openly. Frame as recognition of their value to business.

Cost of Key Person Insurance

Factors Affecting Cost:

Age of Insured

Younger = Lower premiums

Older = Higher premiums

Health Status

Excellent health = Best rates

Health issues = Higher rates or declined

Coverage Amount

Higher coverage = Higher premium (but lower per $1,000)

Policy Type

Term = Lower

Permanent = Higher

Term Length (for term policies)

10-year = Lowest

20-year = Moderate

30-year = Higher

Occupation/Lifestyle

Low-risk = Standard rates

High-risk (pilot, dangerous occupation) = Higher

Rates for healthy, non-smokers. Actual rates vary by insurer and health status.

ROI Perspective:

$1M coverage, 45-year-old, $1,500/year premium:

Cost over 20 years: $30,000

Protection: $1,000,000

Cost per $100,000 coverage: $3,000 over 20 years

If key person dies in year 15:

Total premiums paid: $22,500

Death benefit received: $1,000,000

Return: 4,444%

Even if key person never dies:

Cost: $30,000 over 20 years

Peace of mind: Priceless

Business protection: Invaluable

What to Do Next

This Week:

Identify your key persons using the criteria in this guide

Estimate financial impact of losing each key person

Calculate coverage amounts needed for adequate protection

This Month:

Get quotes from business insurance specialists

Compare term vs. permanent options

Review budget to determine affordable premiums

Discuss with key persons (they must consent and participate)

Within 90 Days:

Purchase policies on key persons

Pass business resolution documenting purpose

Set up premium payments (annual usually most cost-effective)

Integrate into business continuity planning

Get Your Key Person Insurance Quote

Every business with key employees faces this risk. The question isn't whether you should have key person insurance—it's how much coverage you need and when you'll buy it.

Don't wait for tragedy to realize your business was unprotected. One unexpected death can destroy years of hard work and investment.

Contact Pinoy General Insurance Services for:

Free key person analysis (identify your key persons)

Coverage calculation (determine adequate amounts)

Quotes from multiple insurers (term and permanent options)

Policy structure recommendations (term, permanent, or hybrid)

Tax treatment guidance (work with your CPA)

Integration with business succession planning

Located at 17304 Norwalk Blvd, Cerritos, CA 90703, we've been protecting Orange County businesses since 1993. As a founding member of the Artesia Chamber of Commerce, we understand the critical role key employees play in small business success.

We specialize in key person insurance for:

Professional services firms

Family-owned businesses

Technology companies

Manufacturing businesses

Healthcare practices

And more

Call (562) 402-1737 or email info@pinoygeneralinsurance.com for your free key person insurance consultation.

Your key employees are your business's most valuable assets. Protect them—and your business—today.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County businesses protect their operations through comprehensive business insurance solutions, including key person life insurance. Felix specializes in helping business owners identify critical employees, calculate appropriate coverage amounts, and structure key person insurance policies that provide maximum protection at affordable costs.

Pinoy General Insurance Services

17304 Norwalk Blvd

Cerritos, CA 90703

Phone: (562) 402-1737

Email: info@pinoygeneralinsurance.com

Website: pinoygeneralinsurance.com

Founding Member - Artesia Chamber of Commerce

Serving Orange County Since 1993

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.