Pet Insurance: Is It Worth It for Cerritos Pet Owners? (Here's the Math)

Pet insurance can save thousands on veterinary bills—here's what it covers, what it costs, and how to decide if it's worth buying.

SPECIALTY INSURANCEINSURANCE TIPS

Felix | Pinoy General Insurance Services

2/27/20266 min read

Your dog needs emergency surgery. The vet bill: $4,500.

Do you have that money available right now? If not, what do you do?

This is the situation thousands of pet owners face every year. Veterinary costs have increased 60% over the past decade, and emergency procedures routinely exceed $3,000-$10,000.

Pet insurance can protect you from these unexpected costs—but it's not right for everyone. The decision depends on your financial situation, your pet's age and breed, and your risk tolerance.

This guide breaks down exactly what pet insurance covers, what it costs in California, and the math you need to determine whether it's worth buying for your situation.

What Is Pet Insurance?

Pet insurance reimburses you for veterinary expenses when your pet gets sick or injured.

How it works:

You pay the vet bill upfront

You submit a claim to your pet insurance company

They reimburse you based on your coverage level (typically 70-90% after deductible)

It's NOT like health insurance:

You can use any licensed vet (no network restrictions)

Pre-existing conditions are excluded

You pay upfront and get reimbursed (not billed directly)

What Does Pet Insurance Cover?

1. Accident Coverage

Covers injuries from accidents:

Broken bones

Lacerations and wounds

Foreign object ingestion

Poisoning

Car accidents

Bite wounds

Example: Your dog swallows a toy, requires emergency surgery. Cost: $3,200. With 80% reimbursement and $250 deductible, you pay $890, insurance pays $2,310.

2. Illness Coverage

Covers treatment for illnesses:

Cancer

Infections

Digestive issues

Respiratory conditions

Kidney disease

Diabetes

Allergies

Example: Your cat is diagnosed with diabetes, requires ongoing insulin and monitoring. Annual cost: $2,400. With 80% reimbursement, you pay $480/year, insurance pays $1,920/year.

3. Hereditary and Congenital Conditions (If Included)

Many breeds are prone to specific genetic conditions:

Hip dysplasia (German Shepherds, Labradors)

Heart conditions (Cavalier King Charles Spaniels)

Respiratory issues (Bulldogs, Pugs)

Not all policies cover hereditary conditions—verify this before buying.

4. Wellness and Preventive Care (Optional Add-On)

Optional wellness plans cover routine care:

Annual exams

Vaccinations

Dental cleanings

Flea/tick prevention

Spay/neuter

Note: Wellness coverage is usually an add-on that costs $10-$25/month extra.

Is it worth it? Usually no. Routine care is predictable and budgetable. The math rarely works out—you pay $200-$300/year for coverage that reimburses $150-$250 in routine care.

What Pet Insurance Does NOT Cover

❌ Pre-existing conditions

Any illness or injury diagnosed before coverage starts

Conditions during waiting periods (typically 14 days for illness, 2 days for accidents)

❌ Elective procedures

Cosmetic surgeries (tail docking, ear cropping)

Breeding costs

Pregnancy and birth

❌ Grooming

❌ Food and supplements (unless prescribed for a covered condition)

❌ Behavioral training (unless related to a medical condition)

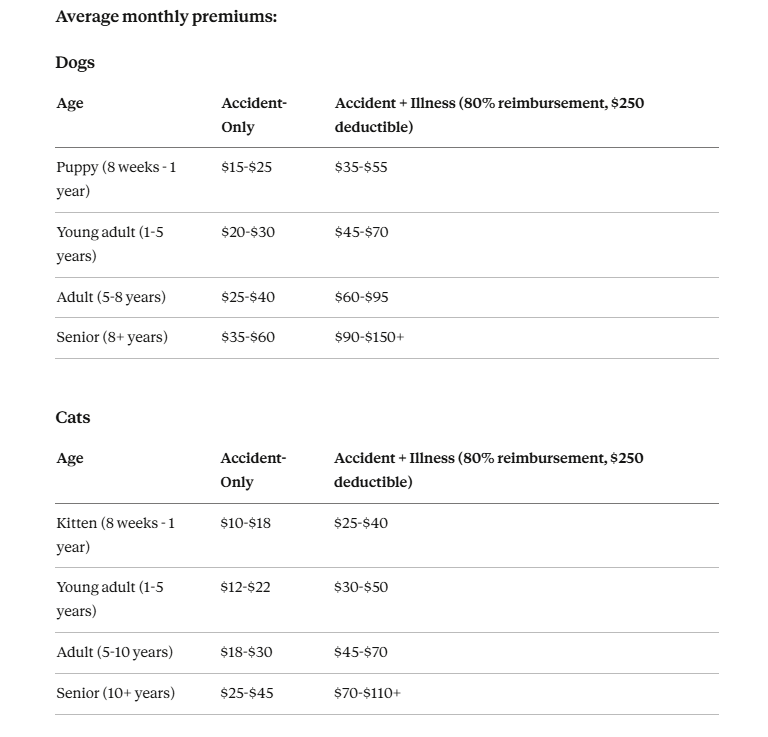

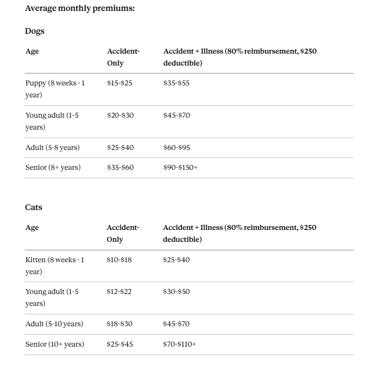

What Does Pet Insurance Cost in California?

Factors that affect cost:

Pet's age (older = more expensive)

Breed (purebreds with known health issues cost more)

Location (California is more expensive than national average)

Coverage level (90% reimbursement costs more than 70%)

Deductible (higher deductible = lower premium)

Annual maximum (unlimited coverage costs more than $10,000 cap)

The Math: Is Pet Insurance Worth It?

This depends on three factors:

Can you afford a $3,000-$8,000 emergency vet bill right now?

Is your pet young and healthy (good candidate) or old with pre-existing conditions (poor candidate)?

Are you disciplined enough to save monthly instead of buying insurance?

Scenario #1: You CAN afford emergency vet bills

Self-insurance strategy:

Don't buy pet insurance

Save $50/month in a dedicated "pet emergency fund"

After 2 years, you have $1,200 saved

After 5 years, you have $3,000 saved

Use this fund for vet emergencies

When this works:

Your pet stays healthy for the first few years

You're disciplined about saving

You have other emergency funds to draw from if needed

When this fails:

Major emergency happens in year 1 before you've saved enough

You're not disciplined about saving

Scenario #2: You CANNOT afford a $5,000 emergency vet bill

Pet insurance makes sense:

Buy accident + illness coverage

Choose 80% reimbursement, $250-$500 deductible

Annual cost: $600-$900 for a young dog, $400-$600 for a cat

If a major emergency occurs, insurance pays 80% of costs

Example:

Emergency surgery: $5,000

Your deductible: $500

Insurance pays 80% of remaining $4,500 = $3,600

You pay: $1,400

Without insurance, you'd pay: $5,000

Scenario #3: High-Risk Breed or Known Health Issues

Breeds prone to expensive conditions:

Bulldogs (respiratory, orthopedic issues)

German Shepherds (hip dysplasia)

Golden Retrievers (cancer)

Dachshunds (back problems)

Great Danes (heart conditions, bloat)

For these breeds, insurance often pays for itself:

Example: Golden Retriever, age 3, diagnosed with cancer. Treatment cost over 2 years: $18,000.

With insurance:

Total premiums paid: $1,200 ($50/month × 24 months)

Deductible per year: $500 × 2 = $1,000

Insurance reimburses: 80% of $17,000 = $13,600

Total out-of-pocket: $1,200 + $1,000 + $3,400 = $5,600

Savings: $12,400

Without insurance:

Total out-of-pocket: $18,000

When to Buy Pet Insurance

✅ Buy Pet Insurance If:

You can't afford unexpected $3,000+ vet bills

Pet insurance converts unpredictable large expenses into predictable monthly premiums

Your pet is young and healthy

No pre-existing conditions to exclude

Lower premiums for young pets

Decades of coverage ahead

You have a purebred with known health risks

Breed-specific conditions are expensive

Insurance covers hereditary conditions (if purchased before diagnosis)

You want peace of mind

You'll never have to choose between your pet's life and your finances

Worth it for emotional security alone

❌ Skip Pet Insurance If:

Your pet is old with pre-existing conditions

Pre-existing conditions won't be covered

Premiums are high for senior pets

Limited benefit period remaining

You have $10,000+ in emergency savings

You can self-insure

Invest the premium savings instead

You're comfortable with risk

You're willing to put a limit on what you'd spend to save your pet

You accept that some conditions may be untreatable due to cost

How to Choose a Pet Insurance Policy

Step 1: Decide on Coverage Type

Accident-only:

Cheapest option

Only covers injuries, not illnesses

Best for: Budget-conscious owners willing to pay for illness out-of-pocket

Accident + Illness:

Covers both accidents and illnesses

Best for: Most pet owners

Accident + Illness + Wellness:

Adds routine care coverage

Usually not worth the extra cost

Step 2: Choose Reimbursement Level

Options: 70%, 80%, or 90%

Higher reimbursement = higher premium

Example:

70% reimbursement: $45/month

80% reimbursement: $55/month

90% reimbursement: $70/month

Recommendation: 80% is the sweet spot—good coverage without excessive premiums.

Step 3: Set Your Deductible

Annual deductible options: $100, $250, $500, $1,000

Higher deductible = lower premium

Example:

$100 deductible: $65/month

$250 deductible: $55/month

$500 deductible: $45/month

Recommendation: Choose the highest deductible you can comfortably afford.

Step 4: Choose Annual Maximum

Options:

$5,000/year

$10,000/year

$20,000/year

Unlimited

Unlimited coverage costs 20-30% more than $10,000 cap

Recommendation: $10,000-$20,000 is adequate for most pets. Unlimited is expensive and rarely needed.

Step 5: Shop Multiple Providers

Top pet insurance companies:

Healthy Paws

Trupanion

Embrace

Nationwide (formerly VPI)

ASPCA Pet Insurance

Pets Best

Figo

Compare:

Premium cost

Reimbursement percentage

Annual maximum

Waiting periods

Hereditary condition coverage

Customer reviews and claim processing speed

Common Pet Insurance Mistakes

Mistake #1: Waiting Until Your Pet Is Old or Sick

Once your pet has a condition, it's pre-existing and won't be covered. Buy insurance while your pet is young and healthy.

Mistake #2: Not Reading the Fine Print on Hereditary Conditions

Some policies exclude breed-specific hereditary conditions. If you have a purebred, verify these are covered.

Mistake #3: Dropping Coverage When Your Pet Is Healthy

If you cancel and your pet later develops a condition, it will be pre-existing when you try to buy coverage again. Keep coverage continuous.

Mistake #4: Not Budgeting for Premium Increases

Pet insurance premiums increase as your pet ages. Budget for 5-10% annual increases.

Mistake #5: Buying Wellness Coverage You Don't Need

Wellness plans rarely provide good value. Save money by budgeting for routine care separately.

Real Stories: When Pet Insurance Saved the Day

Story #1: The Emergency Surgery

Pet: 3-year-old Labrador Retriever, Cerritos

Incident: Swallowed a sock, required emergency surgery to remove intestinal blockage

Cost: $4,800

Insurance: Healthy Paws, 80% reimbursement, $250 deductible

Owner paid: $1,160 ($250 deductible + 20% of remaining $4,550)

Insurance paid: $3,640

Total premiums paid to date: $1,500 (30 months × $50/month)

Net savings: $2,140

Story #2: The Cancer Diagnosis

Pet: 6-year-old Golden Retriever

Diagnosis: Lymphoma, required chemotherapy

Total treatment cost over 18 months: $22,000

Insurance: Trupanion, 90% reimbursement, $500 deductible

Owner paid: $2,700 ($500 deductible + 10% of $22,000)

Insurance paid: $19,800

Total premiums paid: $4,500 (over 6 years at average $62/month)

Net savings: $14,800

Story #3: The Chronic Condition

Pet: 8-year-old cat

Diagnosis: Chronic kidney disease, requires ongoing treatment

Annual treatment cost: $3,200/year for remaining 4 years = $12,800 total

Insurance: Embrace, 80% reimbursement, $250 deductible

Owner pays: $1,000/year deductible + 20% of remaining = $1,590/year × 4 = $6,360

Insurance pays: $6,440

Total premiums paid: $5,400 (over 4 years at $112/month for senior cat)

Roughly break-even, but owner never faced $3,200 bills all at once

The Self-Insurance Alternative

If you decide pet insurance isn't worth it for you, commit to self-insurance:

Step 1: Open a dedicated savings account for pet emergencies

Step 2: Deposit $50-$100/month (the amount you'd pay for insurance)

Step 3: Don't touch this money except for vet emergencies

Step 4: Build to at least $5,000-$10,000

Pros:

You keep the money if your pet stays healthy

No reimbursement hassles

Money earns interest

Cons:

If emergency happens early, you won't have enough saved

Requires discipline to save consistently

No protection against catastrophic costs exceeding your savings

Final Thoughts

Pet insurance isn't for everyone, but it can be a financial lifesaver when your pet faces a major illness or injury.

The key questions:

Can you afford a $5,000-$10,000 vet bill tomorrow?

Would you spend that amount to save your pet?

Is your pet young and healthy (good time to buy)?

If you answered yes to #2 and no to #1, pet insurance is probably worth it.

Have questions about pet insurance or other specialty coverages?

📞 Call: (562) 402-1737

📧 Email: info@pinoygeneralinsurance.com

📍 Visit: 17304 Norwalk Blvd, Cerritos, CA 90703

🌐 Online: pinoygeneralinsurance.com

While we specialize in auto, home, and business insurance, we're happy to discuss pet insurance options and point you toward reputable providers.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Southern California residents protect what matters most—including their furry family members.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.