The Complete Guide to Homeowners Insurance Deductibles

How homeowners insurance deductibles work, choosing the right amount, and strategies to optimize your policy costs.

HOMEBUYERSHOME INSURANCEINSURANCE TIPS

Felix | Pinoy General Insurance Services

3/18/202611 min read

Your homeowners insurance deductible is one of the most important—and most misunderstood—parts of your policy. Choose too low, and you're overpaying on premiums for years. Choose too high, and you're risking financial hardship when you need to file a claim.

After helping thousands of Orange County homeowners optimize their insurance over three decades, I can tell you that most Cerritos homeowners have the wrong deductible. They either:

Chose the default option without understanding the implications

Selected the lowest deductible because it "feels safer"

Never reviewed their deductible choice after their initial purchase

Don't actually understand what a deductible is or how it works

This guide explains everything you need to know about homeowners insurance deductibles—how they work, what your options are, how to choose the right amount, and strategies to optimize your policy costs without exposing yourself to unaffordable out-of-pocket expenses.

What Is a Homeowners Insurance Deductible?

Simple Definition: The amount YOU pay out-of-pocket before your insurance company pays anything on a claim.

How It Works:

Your home suffers $10,000 in covered damage from a fire.

Your deductible: $2,500

You pay: $2,500

Insurance pays: $7,500

Your home suffers $1,800 in covered damage from theft.

Your deductible: $2,500

You pay: $1,800 (entire loss, since it's less than deductible)

Insurance pays: $0

Key Principle: You're responsible for losses up to your deductible amount. The insurance company only pays amounts ABOVE your deductible.

Why Deductibles Exist:

Insurance companies use deductibles to:

Prevent small claims: Filing a $500 claim for minor damage costs the insurance company far more than $500 in administrative costs. Deductibles discourage small claims.

Reduce moral hazard: When people pay part of every loss, they're more careful about preventing damage and less likely to inflate claims.

Lower premiums: By accepting responsibility for smaller losses, you reduce the insurance company's exposure, allowing them to charge lower premiums.

Share risk: Insurance is designed for catastrophic losses you can't afford. Deductibles ensure you share in smaller, manageable losses.

Types of Homeowners Insurance Deductibles

There are two main types of deductibles used in California homeowners insurance:

1. Flat Dollar Amount Deductible

How it works: You pay a specific dollar amount regardless of claim size or home value.

Common options in California:

$500

$1,000

$2,500

$5,000

$10,000

Example:

Home value: $600,000

Deductible: $2,500

Claim: $20,000 fire damage

You pay: $2,500

Insurance pays: $17,500

Pros:

Predictable (you know exactly what you'll owe)

Easier to budget for

Same deductible regardless of claim severity

Standard for most coverages

Cons:

May not keep pace with home value increases

Fixed amount doesn't scale with property value

Most common type in California for standard perils (fire, theft, wind, etc.)

2. Percentage Deductible

How it works: You pay a percentage of your home's insured value (Coverage A).

Common options:

1% of Coverage A

2% of Coverage A

5% of Coverage A

10% of Coverage A

Example:

Home insured for: $600,000 (Coverage A)

Deductible: 2%

Deductible amount: $600,000 × 0.02 = $12,000

Claim: $50,000 wind damage

You pay: $12,000

Insurance pays: $38,000

Pros:

Scales with home value

Automatically adjusts as Coverage A increases

Cons:

Unpredictable dollar amount (depends on Coverage A)

Can be very high for expensive homes

Harder to budget for

Typically used for:

Wind/Hail damage (in some policies)

Hurricane damage (coastal areas)

Earthquake damage (separate earthquake policy)

Percentage deductibles can be shockingly expensive:

$800,000 home with 2% deductible = $16,000 out-of-pocket $1,000,000 home with 5% wind deductible = $50,000 out-of-pocket

Important: Always ask whether your deductible is flat dollar or percentage, especially for wind/hail coverage.

Special Deductibles: Wind/Hail, Hurricane, and Earthquake

In addition to your standard "all other perils" deductible, your policy may have separate, higher deductibles for specific perils:

Wind/Hail Deductible

Some insurance companies in California apply separate, higher deductibles for wind and hail damage.

Typical structure:

Standard deductible (fire, theft, etc.): $1,000

Wind/Hail deductible: 2% or 5% of Coverage A

Why insurers do this: Wind and hail claims can be catastrophic and affect many homes simultaneously. Higher deductibles reduce insurer exposure.

Real Example:

Cerritos home - $700,000 Coverage A

Standard deductible: $2,500

Wind/Hail deductible: 2% = $14,000

Windstorm damages roof: $25,000

Homeowner pays: $14,000 (not $2,500!)

Insurance pays: $11,000

This catches many homeowners by surprise.

What to do:

Check if your policy has separate wind/hail deductible

If it does, understand the dollar amount (calculate the percentage)

Consider whether you can afford it

Shop for policies without separate wind/hail deductible

Hurricane Deductible (Coastal California)

If you're in coastal areas, your policy may have a separate hurricane deductible.

Typical structure:

Separate percentage deductible (often 2-5%)

Only applies when National Weather Service declares hurricane

Can be very expensive

California note: Hurricanes are rare in California, but tropical storms can occur. Check whether your policy distinguishes between these.

Earthquake Deductible

Earthquake coverage requires separate policy or endorsement. Earthquake deductibles are ALWAYS percentage-based and typically very high.

Common earthquake deductibles:

10% of Coverage A (most common)

15% of Coverage A

20% of Coverage A

25% of Coverage A (for lower premium)

Example:

$650,000 home

15% earthquake deductible = $97,500

Major earthquake damage: $250,000

Homeowner pays: $97,500

Insurance pays: $152,500

Earthquake deductibles are shockingly high because:

Earthquake losses are catastrophic

Many homes affected simultaneously

Rebuilding costs surge after major quakes

Insurers need high deductibles to remain solvent

If you carry earthquake insurance, you MUST be prepared to pay $50,000-$150,000+ out-of-pocket for a major claim.

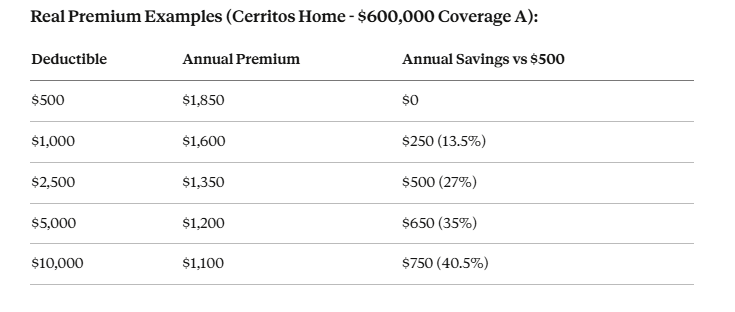

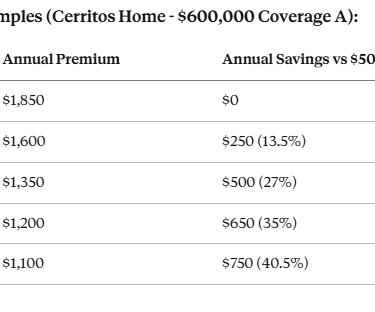

How Deductibles Affect Your Premium

The relationship between deductible and premium is inverse:

Higher deductible = Lower premium

Lower deductible = Higher premium

But the savings aren't linear. Moving from $500 to $1,000 deductible saves more (percentage-wise) than moving from $2,500 to $5,000.

Key Observations:

Biggest savings jump: $500 to $1,000 (saves $250/year)

Diminishing returns: $5,000 to $10,000 only saves $100/year more

Sweet spot for many: $2,500 deductible (good balance of savings and manageable out-of-pocket)

The Math Over Time:

Choosing $2,500 deductible instead of $500:

Annual savings: $500

10-year savings: $5,000

Difference in deductibles: $2,000

If you go 10 years without a major claim, you're ahead $5,000.

If you have one major claim in 10 years:

Extra out-of-pocket: $2,000 (higher deductible)

Premium savings: $5,000

Net benefit: $3,000 ahead

If you have two major claims in 10 years:

Extra out-of-pocket: $4,000

Premium savings: $5,000

Net benefit: $1,000 ahead

You'd need THREE major claims in 10 years to lose money with the higher deductible—and that's before considering the premium increases from filing multiple claims.

How to Choose the Right Deductible

Choosing your deductible isn't about premium savings alone. It's about balancing four factors:

Factor 1: Your Emergency Fund

Golden Rule: Never choose a deductible higher than your emergency fund.

If you have $3,000 in emergency savings, don't choose a $5,000 deductible. You won't be able to afford the out-of-pocket cost if you need to file a claim.

Recommended approach:

Emergency fund $1,000-$2,000: Choose $500-$1,000 deductible

Emergency fund $3,000-$5,000: Choose $1,000-$2,500 deductible

Emergency fund $5,000-$10,000: Choose $2,500-$5,000 deductible

Emergency fund $10,000+: Choose $5,000-$10,000 deductible

Factor 2: Your Risk Tolerance

Some people sleep better knowing they'd only owe $500 out-of-pocket for a claim. Others are comfortable with $5,000 risk in exchange for premium savings.

Questions to ask yourself:

How would I feel paying $1,000 vs $5,000 after a disaster?

Am I comfortable accepting more risk to save money?

Would a high deductible cause financial stress even if I could technically afford it?

Factor 3: Your Home's Condition and Risks

Choose LOWER deductible if:

Your home is older (more likely to have claims)

You live in high-risk area (wildfire zone, flood-prone, etc.)

Your home has known issues (old roof, old plumbing)

You've had claims in the past

You rent out the property (more risk exposure)

Choose HIGHER deductible if:

Your home is newer (less likely to have issues)

Well-maintained property

No known defects or aging systems

Claims-free history

Good neighborhood (low crime/fire risk)

Factor 4: Your Claiming Philosophy

Will you file small claims?

Some homeowners file claims for anything over their deductible. Others only file for truly catastrophic losses.

Consider:

Filing a claim often increases your premium for 3-5 years

Premium increase from one claim can exceed the claim payout

Multiple claims can lead to policy non-renewal

You may want to avoid small claims regardless of deductible

If you plan to only file for major losses (>$10,000), choose a higher deductible and pocket the premium savings.

The Sweet Spot: What Most Homeowners Should Choose

Based on three decades of helping California homeowners, here are my recommendations:

For Most Cerritos Homeowners:

$2,500 deductible

Why this works:

Manageable out-of-pocket for most families with modest savings

Significant premium savings (20-30% vs $500 deductible)

Discourages small claims that hurt you more than help

Affordable enough that you won't delay repairs after loss

Not so low that you're overpaying on premiums

For Well-Funded Homeowners:

$5,000-$10,000 deductible

Who this is for:

Strong emergency fund ($15,000+)

Stable income

Low risk tolerance for premium waste

Plan to only file major claims

Benefits:

Lowest premiums (30-40% savings)

Eliminates temptation to file small claims

Forces self-insurance for minor losses

Maximum long-term savings

For Budget-Conscious or High-Risk Homes:

$1,000 deductible

Who this is for:

Limited emergency savings

Older home with higher claim likelihood

Peace of mind important

Cannot afford large out-of-pocket expense

Benefits:

Lower out-of-pocket if claim occurs

More accessible

Still provides some premium savings vs $500

What to Avoid:

❌ $500 deductible: Rarely makes sense. Premium is high, savings are minimal, and you should avoid filing claims this small anyway.

❌ Deductible higher than emergency fund: You won't be able to afford the claim.

Strategies to Afford a Higher Deductible

Want the premium savings of a higher deductible but worried about affording the out-of-pocket cost? Use these strategies:

Strategy 1: Build Your "Deductible Fund"

Take your annual premium savings and deposit it into a dedicated savings account.

Example:

Switch from $500 to $2,500 deductible

Annual savings: $500

After 5 years: $2,500 in fund (covers entire deductible)

After 10 years: $5,000 in fund

Now you can afford the higher deductible using premium savings, and you keep the extra if you don't claim.

Strategy 2: Gradual Increase

Don't jump from $500 to $5,000 immediately. Increase gradually:

Year 1-2: $1,000 deductible, save premium difference Year 3-4: $2,500 deductible, continue saving Year 5+: $5,000 deductible with strong savings cushion

Strategy 3: Use Home Equity Line of Credit (HELOC)

If you have home equity but limited liquid savings:

Establish HELOC as backup for deductible

Choose higher deductible for premium savings

Only tap HELOC if claim occurs

Pay off quickly from savings/income

Strategy 4: Bundle and Redirect Savings

Bundle home and auto insurance (save 15-25%)

Increase home deductible (save 20-30% more)

Use combined savings to build emergency fund

Within 2-3 years, you'll have cushion for higher deductible

Strategy 5: Consider Payment Plan

Some contractors and restoration companies offer payment plans for deductible amounts. Check before filing claim.

When to Actually File a Claim

Just because damage exceeds your deductible doesn't mean you should file a claim.

File a Claim When: ✅ Damage significantly exceeds deductible (2-3x minimum) ✅ Loss is catastrophic (total loss, major damage) ✅ You cannot afford repairs out-of-pocket ✅ Liability is involved (someone injured on property) ✅ Required by insurance policy (must report certain losses)

Don't File a Claim When: ❌ Damage barely exceeds deductible ❌ You can afford repair ❌ Small loss ($2,000-$5,000) ❌ You've had recent claims already ❌ Near policy renewal (could affect renewal)

Why?

Claims affect premiums for 3-5 years:

One claim: 20-40% premium increase

Two claims: 40-80% premium increase

Three claims: Policy non-renewal likely

Real Example:

$3,000 theft claim with $2,500 deductible

Immediate:

Insurance pays: $500

You pay: $2,500

Next 5 years:

Premium before claim: $1,500/year

Premium after claim: $1,950/year (30% increase)

Extra cost over 5 years: $2,250

Total cost of filing this claim:

Deductible: $2,500

Premium increases: $2,250

Total: $4,750

Insurance payout: $500

You lost $4,250 by filing this claim.

Better decision: Pay the $3,000 out-of-pocket, avoid claim, keep low premiums.

The Rule: Only file claims worth at least 3-5 times your annual premium.

How Deductibles Work with Different Types of Claims

Total Loss Claims:

If your home is destroyed (total loss), your deductible still applies.

Example:

Home insured for $650,000

Total loss from fire

Deductible: $2,500

You receive: $647,500

You still owe the deductible even though you lost everything.

Partial Loss Claims:

Most claims are partial losses (roof damage, kitchen fire, theft, etc.)

Example:

Kitchen fire damage: $35,000

Deductible: $2,500

Insurance pays: $32,500

Liability Claims:

If someone is injured on your property and you're liable, your liability coverage (Coverage E) typically has NO deductible.

Example:

Guest slips and falls

Medical bills: $50,000

Lawsuit settlement: $100,000

Your deductible: $0

Insurance pays: $150,000 (up to your liability limit)

Additional Living Expenses (Coverage D):

If your home is uninhabitable due to covered loss, your ALE coverage typically uses the SAME deductible as your dwelling coverage.

Example:

Fire forces you out of home for 4 months

Hotel and food costs: $12,000

Deductible: $2,500

Insurance pays: $9,500

Other Structures (Coverage B):

Damage to detached garage, shed, fence uses your standard deductible.

Per Occurrence:

Deductibles apply per occurrence, not per item.

Example:

Hail damages roof, windows, and car

Roof: $15,000

Windows: $5,000

(Car covered by auto policy separately)

Total home damage: $20,000

Deductible: $2,500 (once, not per item)

Insurance pays: $17,500

California-Specific Deductible Considerations

Wildfire Risk:

If you live in high-fire-risk area:

Consider LOWER deductible (higher claim likelihood)

Ensure deductible is affordable if evacuated

Review whether fire has separate deductible (rare)

Earthquake Coverage:

California earthquake deductibles are 10-25% of Coverage A.

Recommendation:

If you can afford $75,000-$150,000 out-of-pocket: Get earthquake coverage

If you cannot: Save money in emergency fund instead

FAIR Plan:

If you're in FAIR Plan (high-risk state program):

Deductible options may be limited

Typically higher than standard market

Check what options are available

Brush Clearance Requirements:

Maintaining proper brush clearance around your home can:

Prevent claims (reduces risk)

Allow higher deductible choice

Potentially qualify for discounts

Common Deductible Mistakes

Mistake #1: Choosing Default Without Thinking

Many homeowners select whatever deductible the agent suggests or whatever was on the quote, without analyzing what makes sense for their situation.

Fix: Actively choose deductible based on your emergency fund and risk tolerance.

Mistake #2: Not Knowing What Deductible You Have

Ask a homeowner what their deductible is, and many can't answer.

Fix: Pull out your policy right now and check. Make note of:

Standard deductible amount

Whether it's dollar or percentage

Any special deductibles (wind, earthquake, etc.)

Mistake #3: Percentage Deductible Surprise

Homeowners with percentage deductibles often don't realize the dollar amount until they file a claim.

Fix: Calculate your percentage deductible:

Coverage A × Percentage = Your deductible

Example: $700,000 × 2% = $14,000

Mistake #4: Not Updating After Home Value Increases

If your Coverage A increases (home value rises, you renovate), your percentage deductible increases too.

Fix: Review deductible dollar amount annually if you have percentage deductible.

Mistake #5: Filing Small Claims

Filing claims barely above your deductible costs you more in premium increases than you receive in payout.

Fix: Only file claims worth 3-5x your annual premium.

Mistake #6: Different Deductibles for Home and Auto

Some people have $500 deductible on home but $2,500 on auto (or vice versa) without logical reason.

Fix: Apply same decision-making framework to all insurance deductibles.

What to Do Next

Action Plan:

This Week:

Find your current homeowners insurance policy

Check your deductible (declarations page)

Verify whether it's dollar amount or percentage

Check for special deductibles (wind, earthquake)

Calculate percentage deductibles to know dollar amount

This Month:

Review your emergency fund

Decide if current deductible is appropriate

Get quotes for different deductible amounts

Calculate premium savings

Make change if beneficial

Annually:

Review deductible during policy renewal

Adjust if financial situation changes

Verify Coverage A hasn't increased significantly (affecting percentage deductibles)

Get Your Personalized Deductible Recommendation

Choosing the right homeowners insurance deductible requires balancing premium savings with financial security. There's no one-size-fits-all answer—the right deductible depends on your emergency fund, risk tolerance, home condition, and financial goals.

Contact Pinoy General Insurance Services for:

Free policy review

Deductible analysis and recommendations

Premium quotes at multiple deductible levels

Guidance on building emergency fund

Strategies to optimize total insurance costs

Located at 17304 Norwalk Blvd, Cerritos, CA 90703, we've been helping Orange County homeowners optimize their insurance since 1993. As a founding member of the Artesia Chamber of Commerce, we're committed to helping local residents make smart insurance decisions.

Call (562) 402-1737 or email info@pinoygeneralinsurance.com for your free policy review.

Your deductible is one of the most important decisions in your homeowners insurance. Make sure it's right for you.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County homeowners understand and optimize their insurance coverage, including choosing appropriate deductibles that balance cost savings with financial security. Felix specializes in helping clients make informed decisions about deductibles based on their unique financial situations and risk profiles.

Pinoy General Insurance Services

17304 Norwalk Blvd

Cerritos, CA 90703

Phone: (562) 402-1737

Email: info@pinoygeneralinsurance.com

Website: pinoygeneralinsurance.com

Founding Member - Artesia Chamber of Commerce

Serving Orange County Since 1993

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.