The Complete Guide to Insuring Teen Drivers in California (2026)

Everything California parents need to know about adding teen drivers to car insurance, from costs to discounts to safety strategies.

AUTO INSURANCE

Felix | Pinoy General Insurance Services

3/6/202612 min read

Adding a teenager to your car insurance policy is one of the most expensive parenting milestones you'll face. California parents can expect their auto insurance premiums to increase by 50-100% when they add a teen driver—sometimes even more depending on the vehicle and coverage levels.

But here's the reality: most parents approach teen driver insurance completely wrong. They focus solely on finding the cheapest rate without understanding the coverage gaps, discount opportunities, or safety strategies that could save them thousands while actually protecting their teen better.

After helping hundreds of Cerritos families navigate teen driver insurance since 1993, I've seen the same mistakes repeated over and over. More importantly, I've seen the families who do it right—the ones who save 30-40% through strategic planning while ensuring their teens have proper protection.

This guide covers everything you need to know about insuring teen drivers in California, based on real data, actual premiums, and three decades of experience helping local families.

Why Teen Driver Insurance Costs So Much

Let's start with the uncomfortable truth: teen drivers are genuinely high-risk.

The Statistics Are Sobering:

Drivers aged 16-19 are nearly 3 times more likely to be in a fatal crash than drivers 20 and older (NHTSA data)

Teen drivers have the highest crash rate of any age group in California

25% of teen drivers are involved in an accident within their first year of driving

Motor vehicle crashes are the leading cause of death for U.S. teens

Insurance companies aren't arbitrarily charging you more—they're responding to mathematical risk. Every dollar your premium increases reflects actual claims data showing that teen drivers cost insurers significantly more in payouts.

What Drives Teen Insurance Costs:

Inexperience: Teens simply haven't developed the reflexes, judgment, and hazard recognition that comes with years of driving

Risk-Taking Behavior: Studies show teens are more likely to speed, text while driving, and make impulsive decisions

Brain Development: The prefrontal cortex (responsible for decision-making) isn't fully developed until age 25

Peer Pressure: Teens with other teen passengers have 3x higher crash risk

Night Driving: Fatal crash rates for teen drivers are 3x higher at night

Understanding why insurance is expensive helps you make smarter decisions about coverage, vehicles, and risk management.

How Much Will It Actually Cost?

Here's what real California families are paying to add teen drivers in 2026 (based on our actual client data in Orange County):

Average Premium Increase by Driver Age:

16-year-old driver: $2,400-$3,600/year increase ($200-$300/month)

17-year-old driver: $2,200-$3,400/year increase ($183-$283/month)

18-year-old driver: $2,000-$3,200/year increase ($167-$267/month)

19-year-old driver: $1,800-$2,800/year increase ($150-$233/month)

Factors That Affect Your Specific Cost:

Your actual premium depends on several variables:

The Vehicle They Drive:

Older sedan (Honda Civic, Toyota Corolla): Lower end of range

Newer SUV or sports car: Upper end of range or higher

Vehicle safety features can reduce costs 5-10%

Your Current Insurance Company:

Some insurers specialize in teen drivers and offer better rates

Others penalize teen drivers more heavily

Rate differences can exceed $1,000/year between carriers for identical coverage

Your Location in California:

Urban areas (Los Angeles, San Francisco): Higher rates due to accident density

Suburban areas (Cerritos, Orange County): Moderate rates

Rural areas: Generally lower rates

Your Teen's Gender:

Male teens typically cost 10-20% more than female teens

This gap narrows significantly by age 20-21

Some states have banned gender-based pricing, but California still allows it

Coverage Levels:

Minimum liability (15/30/5): Cheapest but risky

Standard coverage (100/300/100): Moderate cost

Full coverage with low deductibles: Most expensive but best protection

Real Example from a Cerritos Family:

The Martinez Family - 2025 Client

Parents: 2 drivers, clean records, 2019 Honda CR-V and 2021 Toyota Camry

Original premium: $2,400/year ($200/month)

Added 16-year-old son driving the Camry

New premium with teen: $4,900/year ($408/month)

Increase: $2,500/year or $208/month

After shopping 15 carriers and applying all available discounts, we reduced their premium to $3,800/year—a savings of $1,100 annually compared to just adding the teen to their existing policy.

Should You Add Them to Your Policy or Buy Separate Insurance?

This is one of the most common questions we get, and the answer is almost always the same: keep them on your policy.

Why Keeping Teens on Your Policy Usually Saves Money:

Multi-Car Discount: Adding a teen driver usually maintains or increases your multi-car discount

Multi-Policy Discount: Your homeowners/renters insurance bundle discount stays intact

Shared Liability Protection: Your policy's liability limits protect the entire household

Easier Claims Management: One policy means one deductible, one claims process

Administrative Simplicity: One renewal date, one payment, one company to deal with

The Math:

Adding teen to parent's policy: $2,500/year increase (typical)

Separate policy for teen: $4,500-$7,000/year (typical)

Savings by staying on parent's policy: $2,000-$4,500/year

The Only Time a Separate Policy Makes Sense:

Emancipated Minor: Teen lives independently and owns their vehicle

Teen Owns Expensive Vehicle: In rare cases, separating a high-value car can reduce overall costs

Parents Don't Own Vehicles: If parents don't drive and only the teen needs coverage

Excluded Driver Situation: Complex family situations requiring separation of risk

For 99% of California families, keeping teens on the family policy is significantly cheaper.

The Best Way to Add a Teen Driver to Your Policy

Here's the strategic approach that saves our clients the most money:

Step 1: Shop BEFORE Adding Them (3-6 Months Before Their License)

This is the single most important step most parents skip. Here's why it matters:

Once you add a teen to your current policy, switching insurers becomes harder (you're locked in for the policy term)

Different companies treat teen drivers dramatically differently—rate variations of 40-60% are common

Some companies offer "new driver" discounts that expire after the first policy term

You want to start fresh with the best company for teen drivers, not be stuck with whoever you happened to use before

What to Do:

Get quotes from 10-15 insurance companies 6 months before your teen gets their license

Compare identical coverage levels (don't just look at the cheapest option)

Ask specifically about teen driver discounts and programs

Lock in the best rate before adding the teen

Step 2: Choose the Right Vehicle

The car your teen drives has a massive impact on insurance costs. Here's what actually matters:

Best Vehicles for Teen Drivers (Lowest Insurance Costs):

Mid-size sedans 3-7 years old (Honda Accord, Toyota Camry, Mazda 6)

Older compact cars with good safety ratings (Honda Civic, Toyota Corolla)

Mid-size SUVs with strong safety features (Honda CR-V, Toyota RAV4)

Worst Vehicles for Teen Drivers (Highest Insurance Costs):

Sports cars (Mustang, Camaro, anything with a V8)

Brand new vehicles (depreciation risk + high repair costs)

Luxury vehicles (expensive parts, repair costs)

Trucks with high horsepower

Two-door coupes (statistically higher teen accident rates)

The Safety Feature Discount:

Modern vehicles with these features can reduce teen driver premiums by 5-15%:

Forward collision warning

Automatic emergency braking

Lane departure warning

Blind spot monitoring

Electronic stability control

Anti-lock brakes

Real Example:

2016 Honda Civic LX (Safety Features) vs 2015 Ford Mustang V6

Same 17-year-old driver, same coverage

Civic: $3,200/year additional premium

Mustang: $4,800/year additional premium

Difference: $1,600/year just based on vehicle choice

Step 3: Maximize Every Available Discount

Teen driver discounts can reduce your premium by 20-40% if you stack them correctly. Here's what's actually available in California:

Good Student Discount (10-25% savings):

Requires 3.0+ GPA or B average

Must provide report card or transcript

Renewal typically required every 6 months

Applies until age 25 at most companies

Average savings: $400-$800/year

Driver Training Discount (5-15% savings):

Completion of approved driver's education course

Must be state-certified program

Discount typically lasts 3 years

Some companies require both classroom and behind-the-wheel training

Average savings: $200-$500/year

Away at School Discount (10-30% savings):

Student attends college 100+ miles from home

Vehicle remains at home (student doesn't take car to school)

Requires proof of enrollment

Usually requires student to be listed as occasional driver

Average savings: $300-$900/year

This is the biggest discount most parents don't know about. If your teen goes to college without a car, you can reduce their insurance cost by up to 30%.

Defensive Driving Discount (5-10% savings):

Completion of approved defensive driving course

Some companies offer teen-specific programs

May be stackable with driver training discount

Average savings: $150-$350/year

Telematics/Usage-Based Discount (5-30% savings):

Mobile app or device monitors driving behavior

Tracks speed, braking, acceleration, time of day

Good driving habits = increasing discounts over time

Programs: Snapshot (Progressive), Drivewise (Allstate), SmartRide (Nationwide)

Potential savings: $200-$1,000/year

This is controversial among parents: Some see it as invasive surveillance. Others view it as valuable accountability. The financial incentive is real—safe teen drivers can earn substantial discounts.

Stacking Example (Real Client from Norwalk):

Base teen driver cost: $3,200/year

Good student discount (20%): -$640

Driver training discount (10%): -$320

Telematics discount (15%): -$480

Total discounts: $1,440/year

Final cost: $1,760/year (45% savings)

Step 4: Set Clear Coverage Expectations

This is where most parents make expensive mistakes. Let me be direct: do not carry minimum liability coverage with a teen driver.

California Minimum Coverage (15/30/5):

$15,000 per person for bodily injury

$30,000 per accident for bodily injury

$5,000 for property damage

Why This Is Dangerously Low for Teen Drivers:

A teen driver rear-ends another vehicle at a red light. The other driver suffers neck injuries requiring surgery. Medical bills: $85,000. Physical therapy: $15,000. Lost wages: $20,000. Total: $120,000.

Your policy limit: $15,000 per person.

You're personally liable for $105,000.

With teen drivers, the risk of a serious accident causing significant damages is simply too high to carry minimum coverage. One accident can financially devastate your family.

Recommended Coverage for Teen Drivers:

Liability:

Minimum: 100/300/100

Better: 250/500/100

Best: 500/500/100 (surprisingly affordable at these levels)

Additional Protection:

Uninsured/Underinsured Motorist: Match your liability limits

Medical Payments: $5,000-$10,000

Collision: Consider $1,000 deductible on older vehicles

Comprehensive: $500-$1,000 deductible

The Cost Difference Isn't What You Think:

Moving from California minimum (15/30/5) to proper coverage (100/300/100) typically costs only $15-$40/month more—a fraction of the financial risk you're eliminating.

Step 5: Consider a Parent-Teen Driving Contract

The insurance policy protects you financially. A driving contract protects your teen physically.

Key Elements to Include:

Zero Tolerance Rules:

No phone use while driving (even at red lights)

No passengers for first 6-12 months

No driving between 11pm-5am (California law: midnight-5am restriction for first year)

No alcohol/drugs (obviously, but state it explicitly)

Earned Privileges:

Start with daytime, local driving only

Gradually add highway driving, night driving, passengers

Tie expanded privileges to demonstrated safe driving

Consequence System:

First violation: Loss of driving privileges for 1-2 weeks

Second violation: Loss of driving privileges for 1 month

Third violation: Loss of driving privileges for 3-6 months

Ticket/accident: Teen pays insurance increase and deductible

Financial Responsibility:

Teen contributes to gas, insurance, or both

Teen pays for tickets and increases in premium

Teen maintains good grades for discount eligibility

Why This Matters:

Studies show teens with parent-set driving contracts have 30% fewer crashes and 50% fewer traffic violations. The conversation itself—sitting down and going through expectations—creates accountability that reduces risky behavior.

Common Teen Driver Insurance Mistakes to Avoid

After three decades in this business, I've seen these mistakes cost families tens of thousands of dollars:

Mistake #1: Not Listing the Teen Driver

Some parents think they can save money by not formally adding their teen to the policy. This is insurance fraud and can result in:

Denied claims

Policy cancellation

Difficulty getting coverage in the future

Personal liability for all damages

Potential criminal charges

Every insurance company will discover an unlisted teen driver eventually—usually after an accident when it's too late.

Mistake #2: Making Assumptions About "Occasional Driver" Status

"Occasional driver" means your teen drives less than 50% of the time and doesn't have regular access to a vehicle. If your teen:

Has their own car (even if it's titled to you)

Drives to school daily

Has regular use of any household vehicle

They're not an occasional driver—they're a primary or regular driver and must be listed as such.

Mistake #3: Buying a Car in the Teen's Name

Never, ever put a vehicle title in your teen's name. Here's why:

Insurance costs 2-3x more for teen-owned vehicles

Teen becomes personally liable in lawsuits

Harder to maintain family policy discounts

Limited insurance options (many companies won't write policies for teen-owned vehicles)

Keep all vehicles titled to parents until the teen is 21-25 and has established their own insurance history.

Mistake #4: Failing to Re-Shop After the First Year

Teen driver rates vary wildly between companies, and what's cheapest when you add them might not be cheapest a year later. Some companies:

Offer introductory discounts that expire

Increase rates more aggressively after first-year claims

Don't reward good driving as quickly as competitors

Best Practice: Re-shop your teen driver insurance every year for the first 3-4 years. Rate variations of $800-$1,500/year are common between companies for the exact same coverage.

Mistake #5: Prioritizing Price Over Coverage

Yes, teen driver insurance is expensive. But the cheapest policy is rarely the best value. Consider:

Claims service: Will they fight for you or against you?

Financial strength: Will they be around in 5 years?

Coverage limits: Are you actually protected or just insured?

Deductibles: Can you afford the out-of-pocket costs?

A policy that costs $300/year less but fights every claim and provides terrible service isn't saving you money.

Special Situations: What to Do If...

Your Teen Gets a Ticket

First ticket or minor violation:

Premium increase: 15-30% typically

Duration: Usually 3 years

Cost: $400-$800/year additional

Action: Consider traffic school to remove the point (if eligible)

Multiple tickets or serious violations:

Premium increase: 40-80% or more

Risk: Some companies will non-renew your policy

Action: Expect to shop for new coverage, possibly with a high-risk insurer

Your Teen Has an Accident

At-fault accident:

Premium increase: 20-50% depending on damage amount

Duration: 3-5 years typically

Surcharge: Usually kicks in at renewal, not immediately

Action: File a claim for damage above your deductible + 20-30%

Not-at-fault accident:

Most companies won't surcharge

Some companies still increase rates 5-10%

Your claim history still shows the accident

Your Teen Goes to College

Without a car:

Apply for "away at school" discount immediately

Keep them listed as occasional driver

Maintain good student discount with transcripts

Potential savings: 20-30% of their portion of premium

With a car:

Update address to college location (affects rates)

Consider storage insurance if car sits unused

Verify coverage extends to out-of-state (most do)

May need separate policy if more than 6 months away

Your Teen Joins the Military

Active duty service members:

May qualify for military discounts (USAA, Armed Forces Insurance)

Vehicle in storage: Comprehensive-only coverage option

Deployment: Suspension of coverage possible with some insurers

Benefits: Better rates through military-specific companies

When Teen Drivers Become Adults: The Path to Lower Rates

The good news: teen driver rates don't last forever. Here's when costs typically decrease:

Age-Based Rate Reductions:

Age 18: 5-10% decrease

Age 19: 10-15% decrease

Age 21: 15-25% decrease (often when rates drop significantly)

Age 25: 20-35% decrease (full "adult" rates kick in)

Milestone-Based Improvements:

3 years claim-free: 10-20% decrease

5 years licensed: 15-25% decrease

Marriage: 5-15% decrease (yes, married drivers get better rates)

Homeownership: 5-10% decrease

By age 25 with a clean record, your child's insurance costs should be 50-70% lower than they were at age 16.

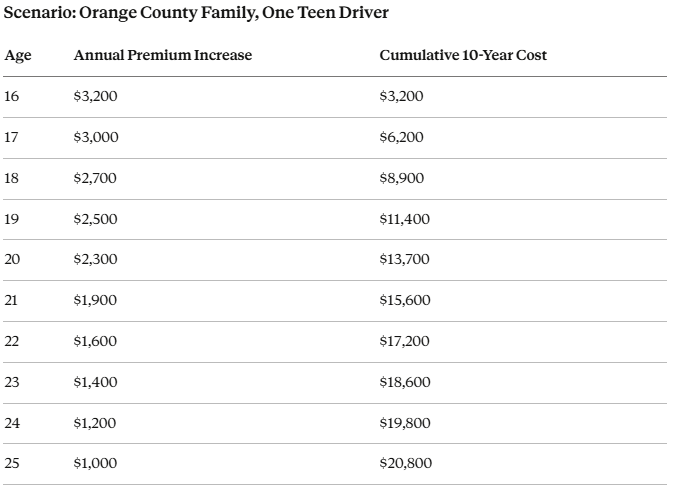

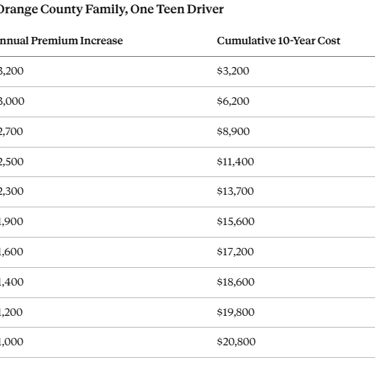

The Bottom Line: What This Costs You in Real Dollars

Let's do the full math for a California family adding a 16-year-old driver and keeping them insured through age 25:

Total cost to insure a teen driver from age 16-25: approximately $20,800

This assumes clean driving record and good student discounts applied. With accidents or tickets, add $5,000-$15,000 to this total.

But here's the critical perspective: That $20,800 over 10 years is the cost of protection. Without insurance:

One serious accident could bankrupt your family

Medical bills alone from injuring another person can exceed $200,000

You'd be personally liable for all damages

Your assets (home, savings, retirement) would be at risk

Teen driver insurance is expensive because teen driving is risky. The insurance doesn't create the risk—it protects you from it.

How Pinoy General Insurance Services Helps Cerritos Families

Since 1993, we've been helping local families navigate the teen driver insurance challenge. Here's our process:

1. Pre-License Consultation (Free)

We meet with families 3-6 months before their teen gets licensed to:

Review your current insurance situation

Explain coverage options and costs

Create a strategic plan for adding the teen driver

Identify every available discount

2. Comprehensive Quote Shopping

We shop your coverage with 15+ insurance companies including:

Major carriers (State Farm, Allstate, Farmers, Nationwide)

Regional specialists (Mercury, CSAA, Wawanesa)

High-value carriers (Chubb, Pure, AIG)

Specialized programs for teen drivers

This isn't about getting you the cheapest policy—it's about finding the best value: the right coverage at the best price with companies that actually pay claims.

3. Discount Maximization

We help you qualify for every available discount:

Good student discount setup and renewal reminders

Driver training course recommendations

Telematics program enrollment and monitoring

Away-at-school verification

Vehicle selection guidance to minimize costs

4. Annual Review & Re-Shopping

Teen driver rates change dramatically year over year. We:

Review your coverage annually

Re-shop with all carriers

Adjust coverage as vehicles and situations change

Track your teen's driving record and address issues immediately

5. Claims Advocacy

If your teen has an accident, we:

Guide you through the claims process

Advocate with the insurance company on your behalf

Manage rate impact and help find alternative coverage if needed

Provide guidance on tickets, accidents, and violations

What to Do Next

If you have a teen driver or will soon, here's your action plan:

Immediate (Today):

Review your current auto insurance policy and coverage limits

Check if your teen qualifies for good student discount (need 3.0+ GPA)

Discuss the teen driving contract concept with your spouse/co-parent

3-6 Months Before License:

Schedule a pre-license consultation with our office

Get comprehensive quotes from 10-15 insurance companies

Identify the best vehicle options for your teen to drive

Enroll teen in driver education course (for discount eligibility)

At License Time:

Add teen to your policy with the best company identified

Implement the parent-teen driving contract

Set up telematics monitoring if available

Provide report cards for good student discount verification

Annually Thereafter:

Re-shop coverage every year for first 3-4 years

Update good student discount with new transcripts

Adjust coverage based on vehicle age and value

Review driving record and address any violations

Get Your Free Teen Driver Insurance Quote

Adding a teen driver to your insurance doesn't have to be overwhelming or overpriced. With proper planning, strategic vehicle selection, and comprehensive discount application, most Cerritos families save $800-$1,500 per year compared to just adding the teen to their existing policy without shopping.

Contact Pinoy General Insurance Services today for:

Free teen driver insurance consultation

Quotes from 15+ insurance companies

Comprehensive discount analysis

Parent-teen driving contract template

Vehicle selection guidance

We're located at 17304 Norwalk Blvd, Cerritos, CA 90703, and we've been helping Orange County families since 1993.

As a founding member of the Artesia Chamber of Commerce, we're deeply connected to our community and committed to protecting local families.

Call us at (562) 402-1737 or email info@pinoygeneralinsurance.com to schedule your free consultation.

Teen driver insurance is one of the most important—and expensive—insurance decisions you'll make. Don't navigate it alone.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County families protect their assets and loved ones through comprehensive insurance solutions. Felix specializes in helping families navigate the teen driver insurance process, with a focus on maximizing discounts and ensuring proper protection.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.