Understanding Actual Cash Value vs. Replacement Cost Coverage

Critical differences between ACV and replacement cost coverage, how each affects your claim payouts, and which is right for your situation.

INSURANCE TIPSHOME INSURANCE

Felix | Pinoy General Insurance Services

3/23/202611 min read

You file a claim after a fire damages your home. The insurance adjuster determines your 10-year-old roof needs complete replacement. Cost: $18,000.

You're expecting an $18,000 check (minus your deductible). Instead, you receive $9,000.

Confused and frustrated, you call your insurance company. They explain: "Your policy provides Actual Cash Value coverage for your roof, not Replacement Cost. We've paid you the depreciated value."

You now owe $9,000 out-of-pocket to replace your roof—money you don't have.

This scenario happens to California homeowners every single day. Most don't understand the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV) coverage until it's too late—until they're holding a claim check that's 40-60% less than they expected.

After helping thousands of Orange County homeowners navigate insurance claims since 1993, I can tell you that understanding ACV vs. RCV is one of the most important—and most misunderstood—aspects of homeowners insurance.

This guide explains exactly what each type of coverage means, how they affect your claim payouts, what they cost, and which one you should have.

What Is Actual Cash Value (ACV)?

Simple Definition: The depreciated value of your property at the time of loss.

Formula: Replacement Cost - Depreciation = Actual Cash Value

How It Works:

Your 10-year-old roof is damaged beyond repair.

Cost to replace with new roof: $18,000 (Replacement Cost)

Depreciation (10 years at 5% per year): $9,000 (50% depreciated)

Actual Cash Value: $9,000

Insurance pays: $9,000 (minus your deductible) You pay out-of-pocket: $9,000 to fully replace the roof

The Concept:

ACV coverage assumes your damaged property had "used" value, not new value. You're compensated for what the item was worth immediately before the loss—accounting for age, wear and tear, and condition.

Think of it like selling a used car:

You bought a car for $30,000 ten years ago

Today it's worth $8,000 (depreciated)

If it's totaled, you get $8,000, not $30,000

ACV insurance works the same way

How Depreciation Is Calculated:

Insurance companies use depreciation schedules based on:

1. Expected Useful Life

Roof: 15-25 years (depending on material)

HVAC: 15-20 years

Water heater: 8-12 years

Appliances: 10-15 years

Carpet: 5-10 years

Paint: 3-7 years

2. Age of Item

5-year-old roof with 20-year life expectancy = 25% depreciated

10-year-old HVAC with 20-year life = 50% depreciated

8-year-old water heater with 10-year life = 80% depreciated

3. Condition

Well-maintained items depreciate slower

Neglected items depreciate faster

Damage accelerates depreciation

Real ACV Claim Example:

Cerritos Home - Kitchen Fire Damage

Items Damaged:

Kitchen cabinets (8 years old)

Countertops (8 years old)

Flooring (8 years old)

Appliances (5-7 years old)

Paint (6 years old)

Replacement Costs:

Cabinets: $12,000

Countertops: $4,000

Flooring: $3,500

Appliances: $6,000

Paint/prep: $2,500 Total Replacement Cost: $28,000

ACV Calculation (40-60% depreciation):

Cabinets: $12,000 - 50% = $6,000

Countertops: $4,000 - 50% = $2,000

Flooring: $3,500 - 60% = $1,400

Appliances: $6,000 - 40% = $3,600

Paint: $2,500 - 50% = $1,250 Total ACV Payout: $14,250

With $1,000 deductible:

Insurance pays: $13,250

Homeowner needs to replace everything: $28,000

Out-of-pocket cost: $14,750

The homeowner expected insurance to cover most of the damage. Instead, they're covering more than half themselves.

What Is Replacement Cost Value (RCV)?

Simple Definition: The cost to replace or repair your property with new items of similar kind and quality, with NO deduction for depreciation.

Formula: Replacement Cost = Actual Cash Value + Depreciation

How It Works:

Your 10-year-old roof is damaged beyond repair.

Cost to replace with new roof: $18,000

Depreciation: Does NOT apply with RCV

Insurance pays: $18,000 (minus your deductible)

With $2,500 deductible:

Insurance pays: $15,500

You pay: $2,500 (only your deductible)

The Concept:

RCV coverage returns you to your pre-loss condition by paying the full cost to replace damaged items with new ones. You're not penalized for the age of your property.

Important: RCV Usually Involves Two Payments

Payment #1 - Actual Cash Value (Immediate): When you file the claim, insurance pays ACV immediately (replacement cost minus depreciation).

Payment #2 - Depreciation "Holdback" (After Repairs): After you actually replace or repair the damaged items, insurance pays the depreciation amount they withheld.

Why this two-step process? Insurance companies want proof you actually replaced the items before paying full replacement cost. This prevents people from pocketing depreciation money without making repairs.

Real RCV Claim Example:

Same Cerritos kitchen fire from above, but with RCV coverage

Immediate Payment (ACV): Insurance pays: $14,250 - $1,000 deductible = $13,250

Homeowner Replaces Everything: Total spent: $28,000

Depreciation Holdback Payment: Insurance pays additional: $13,750 (the depreciation amount)

Final Accounting:

Total insurance payout: $27,000 ($13,250 ACV + $13,750 depreciation)

Total repair cost: $28,000

Homeowner out-of-pocket: $1,000 (just the deductible)

This is how insurance should work—you pay your deductible, insurance pays the rest.

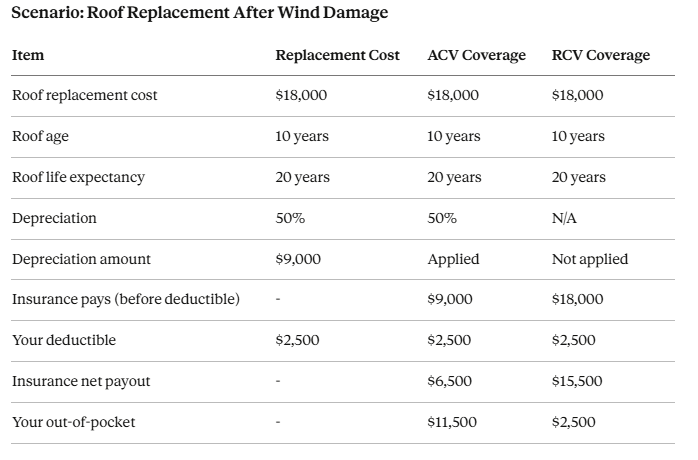

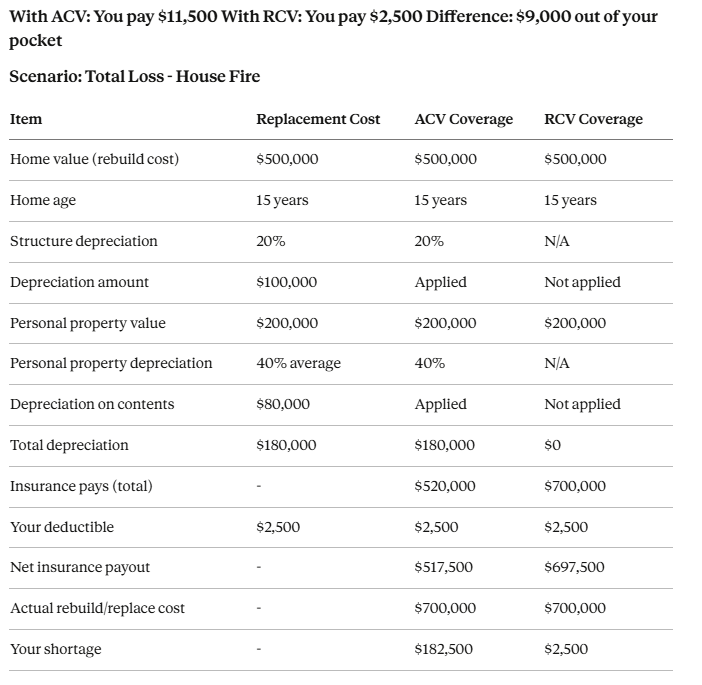

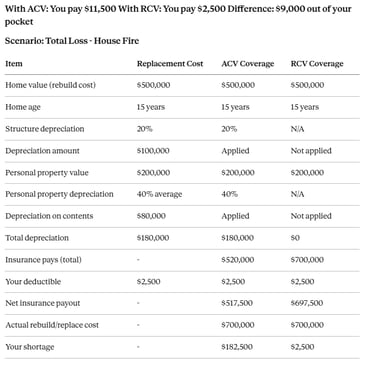

Side-by-Side Comparison: ACV vs. RCV

Let's look at identical claims under each coverage type:

With ACV: You're $182,500 short With RCV: You're covered (minus deductible)

This is why ACV coverage is dangerous for total losses.

When Each Type of Coverage Makes Sense

Replacement Cost Value (RCV) Is Right For:

✅ Primary residence (almost always)

Largest asset most people own

Cannot afford significant out-of-pocket costs for repairs

Want full protection and complete recovery after loss

Standard for most homeowners insurance

✅ Newer homes

Even with less depreciation, RCV provides better protection

Ensures you can fully repair/replace without financial strain

✅ Valuable personal property

Electronics, furniture, appliances add up quickly

Depreciation on contents can be 40-60%

RCV coverage essential for full recovery

✅ Homes with replacement cost over $300,000

Any significant loss creates large depreciation amounts

Cannot risk being undercompensated

✅ Homeowners with limited savings

Cannot afford to cover depreciation gap out-of-pocket

RCV provides predictable, affordable recovery

Actual Cash Value (ACV) Might Make Sense For:

⚠️ Rental/investment properties (sometimes)

Lower premium may align with investment strategy

Owner has capital reserves to cover gaps

Property generates income to fund shortfalls

BUT: Even here, RCV often better choice

⚠️ Vacation homes (rarely)

If owner has significant reserves

If willing to accept lower claim payouts

CAUTION: Most lenders require RCV coverage

⚠️ Very specific roof-only situations

Old roof near end of life (replacing soon anyway)

Willing to accept ACV for lower premium on roof only

NOTE: This should be specific roof endorsement, not whole policy

Who Should NEVER Have ACV Coverage:

❌ Primary residence homeowners ❌ Anyone with a mortgage (lenders typically require RCV) ❌ Homeowners with limited emergency savings ❌ Homes in high-risk areas (fire, wind, hail) ❌ Older homes (more depreciation = larger gaps)

The Bottom Line:

For 95%+ of California homeowners, Replacement Cost coverage is essential. The premium difference is small compared to the massive financial protection difference.

How Much More Does RCV Cost?

The Surprising Answer: Not Much

Typical Premium Difference:

ACV coverage premium: $1,200/year

RCV coverage premium: $1,400-1,500/year

Additional cost: $200-300/year ($17-25/month)

The ROI Analysis:

Scenario 1: No Claims in 20 Years

Extra premium paid for RCV: $4,500 over 20 years

Financial loss: $4,500

BUT: You had peace of mind and protection for 20 years

Scenario 2: One Major Claim in 20 Years

Extra premium paid for RCV: $4,500

Savings from RCV vs ACV on claim: $40,000-$100,000

Net benefit: $35,500-$95,500

Scenario 3: Total Loss

Extra premium paid: $4,500 (assume 20 years)

Savings from RCV vs ACV: $150,000-$200,000

Net benefit: $145,500-$195,500

You're "betting" $225/year that you might need full replacement coverage. The potential payout is 200-800 times your annual bet. This is excellent insurance value.

Special Situations: Roof Coverage

Many California homeowners have RCV coverage on their dwelling but ACV coverage on their roof due to age or insurer requirements.

How Roof-Only ACV Works:

Your policy states: "Replacement Cost coverage except roof is ACV if over 15 years old."

15-year-old roof damaged by wind:

Replacement cost: $18,000

Roof depreciation: 75% (15 years of 20-year life)

ACV payout: $4,500

Your deductible: $2,500

Net insurance payout: $2,000

You owe out-of-pocket: $16,000

This is why roof age matters when shopping for insurance.

Insurer Roof Age Requirements:

Many California insurers now have roof age restrictions:

Common Requirements:

Roof under 15 years: Full RCV coverage

Roof 15-20 years: ACV coverage only

Roof over 20 years: Coverage may be declined or excluded

What This Means:

If you're buying/refinancing a home with an old roof:

You may be required to replace roof before coverage

Or accept ACV coverage (and risk large out-of-pocket costs)

Or pay significantly higher premiums

Strategy:

If your roof is approaching 15 years:

Get inspection to document condition

Replace proactively before age restriction kicks in

Maintain detailed maintenance records

Some insurers offer RCV if roof is well-maintained despite age

Extended Replacement Cost and Guaranteed Replacement Cost

Beyond standard RCV, there are two enhanced options:

Extended Replacement Cost (ERC)

What it is: Coverage that pays ABOVE your dwelling limit (Coverage A) by a specific percentage.

Common options:

125% of Coverage A

150% of Coverage A

Example:

Coverage A (dwelling): $500,000

Extended Replacement Cost: 125%

Maximum payout: $625,000

When you need it: After major disasters, rebuilding costs surge due to:

Labor shortages (contractors in high demand)

Material shortages (lumber, roofing, fixtures)

Building code upgrades (new codes since home was built)

Real Scenario:

California wildfire destroys neighborhood

Your Coverage A: $500,000

Actual rebuild cost (surge pricing + code upgrades): $575,000

Without ERC:

Insurance pays: $500,000

You owe: $75,000

With 125% ERC:

Insurance pays: $575,000 (within 125% limit)

You owe: $0 (beyond deductible)

Cost: Typically adds 5-15% to premium ($75-200/year for most homes)

Guaranteed Replacement Cost (GRC)

What it is: Coverage that pays UNLIMITED amount to rebuild your home to pre-loss condition, regardless of Coverage A amount.

No caps, no limits—full replacement guaranteed.

Example:

Coverage A: $500,000

Actual rebuild cost after disaster: $750,000

GRC coverage pays: $750,000 (full amount)

Requirements:

Home must be insured to 100% of estimated replacement cost

Annual inflation adjustments required

Home must meet underwriting standards

Usually only available for homes under 20-30 years old

Cost: Typically adds 10-25% to premium ($150-350/year for most homes)

Availability:

GRC has become rare in California due to wildfire risks. Many insurers have:

Eliminated GRC options

Limited to specific areas

Restricted to newer homes only

If available, GRC is the gold standard of coverage—but increasingly hard to find.

How to Verify What Coverage You Have

Step 1: Find Your Declarations Page

This is the summary page of your policy showing:

Coverage amounts

Coverage types

Deductibles

Premium

Step 2: Look for Coverage A (Dwelling Coverage)

Find the section describing your dwelling coverage. Look for language like:

Replacement Cost Coverage:

"We will pay the cost to repair or replace with material of like kind and quality"

"Settlement based on replacement cost"

"No deduction for depreciation"

Actual Cash Value Coverage:

"We will pay the actual cash value of the damaged property"

"Settlement based on actual cash value"

"Replacement cost less depreciation"

Step 3: Check Coverage C (Personal Property)

Your dwelling might have RCV while your personal property has ACV. Check both.

Look for:

"Personal Property at Replacement Cost" = RCV

"Personal Property at Actual Cash Value" = ACV

Step 4: Check for Special Limitations

Look for endorsements or special provisions like:

"Roof coverage limited to ACV if over X years old"

"Certain items covered at ACV: [list]"

"Extended Replacement Cost: X%"

Step 5: When in Doubt, Call Your Agent

Ask specifically:

"Do I have Replacement Cost or Actual Cash Value coverage on my dwelling?"

"Do I have Replacement Cost or Actual Cash Value coverage on my personal property?"

"Are there any items covered at ACV instead of RCV?"

"Do I have Extended or Guaranteed Replacement Cost?"

Get written confirmation of your coverage type.

How to Switch from ACV to RCV

If you discover you have ACV coverage, switching to RCV is usually straightforward:

Step 1: Contact Your Insurance Company or Agent

Request to change from ACV to RCV coverage.

Step 2: Provide Any Required Information

Some insurers may require:

Home inspection (for older homes)

Roof inspection (if roof is older)

Updated photos

Verification of home value/replacement cost

Step 3: Review Premium Increase

Agent will quote new premium with RCV coverage.

Typical increase: $200-400/year for most homes

Step 4: Accept and Implement

Once you accept, change usually effective immediately or at next renewal.

Important: Don't cancel ACV coverage before RCV coverage is confirmed in place. Maintain continuous coverage.

Step 5: Verify Change in Writing

Request updated declarations page showing RCV coverage.

Confirm:

Coverage A shows RCV

Coverage C (if applicable) shows RCV

No special limitations or endorsements reducing coverage

California-Specific Considerations

Wildfire Rebuilding Costs:

After major California wildfires (Paradise, Santa Rosa, etc.), rebuilding costs surged 30-50% due to:

Massive contractor demand

Material shortages

New fire-resistant building codes

Labor rate increases

Homeowners with ACV coverage were devastated:

Home replacement cost: $450,000

ACV payout (20% depreciation): $360,000

Actual rebuild cost (with surge): $580,000

Homeowner shortage: $220,000

Many never rebuilt and lost their homes permanently.

Lesson: In California's high wildfire risk areas, RCV + Extended Replacement Cost is essential.

Code Upgrade Requirements:

California frequently updates building codes for:

Fire resistance

Earthquake resistance

Energy efficiency

Water conservation

When rebuilding, you must meet CURRENT codes, not codes from when home was built.

Code upgrades can add:

$20,000-$50,000 for fire-resistant materials

$15,000-$40,000 for seismic upgrades

$10,000-$30,000 for energy efficiency

RCV coverage doesn't automatically cover code upgrades. You need "Ordinance or Law" coverage (separate endorsement).

Recommend: RCV + Extended Replacement Cost + Ordinance or Law coverage

Inflation and Building Costs:

California construction costs increase 4-6% annually. Your Coverage A should increase annually to keep pace.

With ACV coverage:

Your coverage increases, but depreciation also accumulates

Gap between ACV and RCV widens over time

With RCV coverage:

Coverage increases maintain replacement cost protection

Your coverage remains adequate

Make sure your policy includes annual inflation adjustment (most do automatically).

Common Mistakes Homeowners Make

Mistake #1: Not Knowing What Coverage They Have

Most homeowners can't answer: "Do you have ACV or RCV coverage?"

Consequence: Shock and financial hardship at claim time.

Fix: Check your policy TODAY.

Mistake #2: Choosing ACV to Save $200/Year

Saving $200 annually seems smart until you face $50,000+ shortfall after a claim.

Consequence: Cannot afford to fully repair/replace property.

Fix: Prioritize proper coverage over minimal premium savings.

Mistake #3: Assuming All Insurance Is the Same

"I have homeowners insurance" doesn't mean you have adequate coverage.

Consequence: Dangerously underinsured without realizing it.

Fix: Understand your specific coverage types and limits.

Mistake #4: Not Understanding the Two-Payment Process

With RCV, you receive ACV first, then depreciation after repairs completed.

Consequence: Homeowners think they're undercompensated until second payment explained.

Fix: Understand you must complete repairs to receive full RCV payment.

Mistake #5: Accepting ACV for Roof Without Understanding Impact

"Your roof is covered at ACV" sounds fine until you face $15,000 out-of-pocket cost.

Consequence: Unaffordable roof replacement after damage.

Fix: Calculate what ACV means in dollars, not just percentages.

Mistake #6: Not Reviewing Coverage After Roof Replacement

You replace your 20-year-old roof. Your policy still shows ACV for roof.

Consequence: New roof still covered at ACV instead of RCV.

Fix: Notify insurer of roof replacement and request RCV coverage.

What to Do Next

This Week:

Find your homeowners insurance policy

Locate the declarations page

Check Coverage A and Coverage C

Verify whether you have ACV or RCV

If ACV: Call your agent immediately to switch

This Month:

If you have RCV: Verify no special limitations (roof age, etc.)

Check if you have Extended or Guaranteed Replacement Cost

Verify your Coverage A amount is adequate (replacement cost estimate)

Consider adding Ordinance or Law coverage if you don't have it

Review annually to ensure coverage keeps pace with rebuilding costs

Annual Review Checklist:

□ Coverage A still adequate for full replacement? □ Still have RCV coverage (hasn't changed)? □ Any new age restrictions on roof or other items? □ Extended Replacement Cost percentage still appropriate? □ Inflation adjustments being applied?

Get Your Free Policy Review

Understanding whether you have Actual Cash Value or Replacement Cost coverage is one of the most critical aspects of homeowners insurance—yet most homeowners have no idea which they have until disaster strikes.

Don't discover you're underinsured at claim time. Find out now, while you can still make changes.

Contact Pinoy General Insurance Services for:

Free policy review (ACV vs RCV analysis)

Coverage adequacy assessment

Quote comparison if switching insurers

Extended/Guaranteed Replacement Cost options

Ordinance or Law coverage recommendations

Annual review and adjustment guidance

Located at 17304 Norwalk Blvd, Cerritos, CA 90703, we've been protecting Orange County homeowners since 1993. As a founding member of the Artesia Chamber of Commerce, we're committed to ensuring local residents understand their coverage and have proper protection.

Call (562) 402-1737 or email info@pinoygeneralinsurance.com for your free policy review.

The difference between ACV and RCV coverage could mean tens of thousands of dollars out of your pocket. Make sure you have the right coverage.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County homeowners understand their insurance coverage and ensure they have adequate protection for their homes and belongings. Felix specializes in helping homeowners navigate complex insurance terms like ACV and RCV to make informed decisions about their coverage.

Pinoy General Insurance Services

17304 Norwalk Blvd

Cerritos, CA 90703

Phone: (562) 402-1737

Email: info@pinoygeneralinsurance.com

Website: pinoygeneralinsurance.com

Founding Member - Artesia Chamber of Commerce

Serving Orange County Since 1993

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.