Workers' Compensation Insurance in California: What Every Employer Must Know

California requires workers' comp for nearly all employees—here's what it covers, what it costs, and how to avoid costly penalties.

BUSINESS INSURANCEINSURANCE TIPS

Felix | Pinoy General Insurance Services

2/25/20267 min read

If you employ even one person in California—full-time, part-time, or temporary—you're legally required to carry workers' compensation insurance.

No exceptions. No excuses. One employee = mandatory workers' comp.

Yet thousands of California businesses operate without it, either because they don't know they need it or because they're trying to avoid the cost. The penalties for non-compliance are severe: fines up to $100,000, criminal charges, and personal liability for employee injuries.

At Pinoy General Insurance, we help Cerritos and Orange County businesses navigate workers' comp requirements, find affordable coverage, and implement safety programs that reduce claims and premiums.

This guide covers everything employers need to know about workers' compensation in California: what it covers, who needs it, what it costs, and how to stay compliant.

What Is Workers' Compensation Insurance?

Workers' compensation (workers' comp) is insurance that provides benefits to employees who are injured or become ill due to their job.

It covers:

Medical expenses for work-related injuries or illnesses

Lost wages while the employee recovers

Permanent disability benefits if the employee can't return to work

Death benefits to the employee's dependents

In exchange, employees give up the right to sue their employer for workplace injuries (with rare exceptions for intentional harm or gross negligence).

Who Needs Workers' Compensation Insurance in California?

California law requires workers' comp if you have even ONE employee.

This includes:

Full-time employees

Part-time employees

Temporary or seasonal employees

Minors (even family members under 18)

Undocumented workers (yes, they're covered)

Types of businesses that need workers' comp:

Retail stores

Restaurants and food service

Construction and contractors

Professional services (law firms, accounting firms, consultants)

Healthcare providers

Manufacturers

Warehouses and distribution

Offices and administrative businesses

Who Is Exempt?

Very few categories are exempt from California workers' comp requirements:

Sole proprietors with NO employees

If you're the only person working in your business, you don't need workers' comp (though you can buy it voluntarily)

Business partners (in a partnership with no employees)

Partners can opt out of coverage for themselves

Independent contractors (if properly classified)

True independent contractors are not covered under your workers' comp

Warning: Misclassifying employees as independent contractors is illegal and results in massive penalties

Corporate officers who own 15%+ of stock

Can opt out by filing specific paperwork

Certain real estate agents and direct sellers

If they meet specific criteria

Important: When in doubt, assume you need workers' comp. The penalties for non-compliance far outweigh the cost of coverage.

What Does Workers' Compensation Cover?

1. Medical Expenses

Covered:

Doctor visits and hospital care

Surgery and medications

Physical therapy and rehabilitation

Medical equipment (crutches, wheelchairs, etc.)

Ongoing treatment for permanent injuries

No deductible, no copay for the employee. Workers' comp pays 100% of reasonable and necessary medical expenses.

2. Temporary Disability Benefits

If an employee can't work while recovering, workers' comp pays a portion of lost wages.

Payment amount: Typically 2/3 of average weekly wages, subject to minimums and maximums

California 2026 rates:

Minimum: $230.95/week

Maximum: $1,619.15/week

Example:

Employee earns $1,200/week

Injured, can't work for 8 weeks

Workers' comp pays: $800/week × 8 = $6,400

3. Permanent Disability Benefits

If an employee suffers a permanent impairment that affects their ability to work, they receive permanent disability benefits.

Payment calculation: Based on:

Percentage of permanent impairment (determined by doctor)

Employee's age and occupation

Pre-injury wages

Payments: Weekly payments for a specified number of weeks (or lump sum settlement)

4. Supplemental Job Displacement Benefits

If an employee can't return to their previous job due to injury, workers' comp provides vouchers ($6,000-$10,000) for:

Retraining or skill enhancement

Job placement services

5. Death Benefits

If an employee dies from a work-related injury or illness, workers' comp pays:

Funeral expenses (up to $10,000)

Ongoing payments to dependents ($250,000 minimum, up to life expectancy calculations)

What Workers' Compensation Does NOT Cover

❌ Injuries occurring outside of work

Employee injured in a car accident on personal time

❌ Self-inflicted injuries

Suicide, intentional self-harm

❌ Injuries while intoxicated or on illegal drugs

Exception: If intoxication/drug use didn't cause the injury

❌ Injuries during commission of a crime

❌ Injuries sustained while violating company policy

Exception: Minor policy violations don't disqualify claims

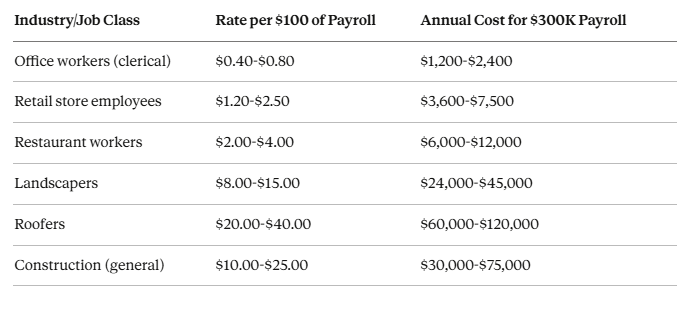

What Does Workers' Compensation Insurance Cost?

Cost varies dramatically based on:

Industry and job classifications

Payroll amount

Claims history

Location

Cost formula:

(Payroll ÷ $100) × Rate per $100 of payroll

Example:

Annual payroll: $300,000

Rate for office workers: $0.40 per $100 of payroll

Cost: ($300,000 ÷ $100) × $0.40 = $1,200/year

Industry Rate Examples (California 2026)

Key takeaway: Higher-risk industries pay significantly more.

Factors That Increase Cost

✅ High-risk industry (construction, roofing, manufacturing)

✅ Claims history (more claims = higher premiums)

✅ Poor safety record

✅ High employee turnover

✅ Misclassified job codes (if you classify roofers as office workers to save money, you'll face massive penalties and back premiums)

Factors That Reduce Cost

✅ Low claims history (3+ years claims-free)

✅ Safety programs (documented training, safety equipment)

✅ Experience modification factor below 1.0 (industry calculation of your claims vs. expected claims)

✅ Accurate job classifications

✅ Return-to-work programs (getting injured employees back to light duty ASAP reduces lost-time claims)

Penalties for Not Having Workers' Comp

California aggressively enforces workers' comp requirements.

Penalties if caught without coverage:

Civil Penalties:

$10,000 minimum fine (even if you have zero employees)

Up to $100,000 in fines

$1,500-$5,000 penalty per employee per day without coverage

Criminal Penalties:

Misdemeanor charges

Up to 1 year in jail

Additional fines up to $250,000

Personal Liability for Employee Injuries:

If an employee is injured and you don't have workers' comp, you're personally liable for all medical bills, lost wages, and damages

Employees can sue you directly (they normally can't sue if you have workers' comp)

No cap on damages

Stop Work Order:

The state can shut down your business until you obtain coverage

Real scenario: Cerritos restaurant owner operated for 2 years without workers' comp (4 employees). Employee suffered severe burn injury in the kitchen. Medical bills: $180,000. Lost wages: $45,000. Restaurant owner didn't have workers' comp.

Outcome:

Personally liable for $225,000 (no insurance to pay)

State fined him $85,000 for operating without workers' comp

Had to sell the restaurant to pay judgments and fines

Declared personal bankruptcy

The cost of workers' comp he was trying to avoid: $8,000/year.

How to Buy Workers' Compensation Insurance

Step 1: Gather Employee and Payroll Information

You'll need:

Total annual payroll

Number of employees

Job classifications for each employee

Business description

Step 2: Get Accurate Job Classifications

Workers' comp rates are based on job codes that describe what employees actually do.

Common mistakes:

Restaurant owner classifies cooks as "office workers" to get lower rates (fraud)

Contractor classifies all workers under one code instead of separating office staff from field workers

Action: Work with your agent to ensure accurate classifications.

Step 3: Shop Multiple Carriers

Workers' comp pricing varies significantly by carrier.

Options:

Standard admitted carriers (Hartford, Travelers, Zurich, Liberty Mutual)

State Fund (California's state-run workers' comp carrier—often the option of last resort for high-risk businesses)

Assigned Risk Pool (for businesses that can't get coverage elsewhere)

Shop at least 3 carriers or work with an independent agent who can compare multiple options.

Step 4: Implement Safety Programs

Carriers offer premium credits (5-15% discounts) for documented safety programs:

Employee safety training

Written safety policies

Personal protective equipment (PPE) requirements

Incident reporting procedures

Step 5: Purchase Policy and Stay Compliant

Once you buy coverage:

Post required workers' comp notice in the workplace (carrier provides this)

Train employees on how to report injuries

Report all injuries to your carrier immediately

Maintain accurate payroll records

How to Reduce Workers' Comp Costs

Strategy #1: Implement a Return-to-Work Program

Getting injured employees back to light-duty work ASAP reduces lost-time claims and premiums.

How it works:

Employee injures their back, can't do heavy lifting

Instead of full disability, they return to light-duty (answering phones, data entry, etc.)

Workers' comp pays partial disability instead of full disability

Employee heals while earning income, claim costs are lower

Savings: 20-40% reduction in claim costs

Strategy #2: Improve Workplace Safety

Fewer injuries = lower claims = lower premiums.

Actions:

Provide safety training

Supply proper safety equipment

Enforce safety policies

Conduct regular safety audits

Savings: 10-25% premium reduction over 3 years

Strategy #3: Manage Claims Proactively

Report all injuries immediately and work with your carrier to manage claims effectively.

Why this matters:

Delays in reporting increase claim costs

Early intervention reduces medical expenses

Proactive claims management improves your experience mod (the factor that affects future premiums)

Strategy #4: Audit Your Payroll Classifications Annually

As your business changes, job classifications may change. Ensure you're classified accurately—overpaying for wrong classifications is common.

Strategy #5: Shop Your Policy Every 2-3 Years

Workers' comp rates are competitive. Shopping carriers regularly ensures you're getting the best price.

Common Workers' Comp Mistakes California Employers Make

Mistake #1: Classifying Employees as Independent Contractors

Why employers do this: Avoid paying workers' comp and payroll taxes.

Why it's illegal: California has strict tests for independent contractor classification (AB5 and subsequent legislation).

Penalties:

Back premiums for all years you should have had coverage

Fines and penalties from the state

Personal liability for injuries to misclassified workers

Potential criminal charges

Mistake #2: Not Reporting Injuries Immediately

California law: Employers must report serious injuries within 5 days.

Why delays are costly:

Claim costs increase

State may penalize you for late reporting

Employee trust erodes

Mistake #3: Trying to Discourage Employees from Filing Claims

Illegal actions:

Threatening to fire employees who file claims

Offering cash payments to avoid filing

Retaliating against employees who file

Penalties:

Serious fines and penalties

Lawsuits for retaliation

Increased state scrutiny

Better approach: Focus on prevention and return-to-work programs, not discouraging legitimate claims.

Mistake #4: Not Posting Required Notices

California requires employers to post workers' comp notices in the workplace. Failure to post can result in fines.

Required posters:

Notice to Employees - Workers' Compensation Rights

Other state and federal labor law posters

Final Thoughts

Workers' compensation insurance isn't optional in California. If you have employees, you must have coverage—no exceptions.

The cost may seem high, but the penalties for non-compliance are catastrophic. And the right coverage protects both your employees and your business from financial disaster.

Need help with workers' compensation insurance?

📞 Call: (562) 402-1737

📧 Email: info@pinoygeneralinsurance.com

📍 Visit: 17304 Norwalk Blvd, Cerritos, CA 90703

🌐 Online: pinoygeneralinsurance.com

We'll help you:

Determine your exact workers' comp requirements

Get accurate job classifications

Compare quotes from multiple carriers

Implement safety programs that reduce premiums

Stay compliant with California law

Because protecting your employees shouldn't put your business at risk.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County businesses protect their property, liability, and income through comprehensive commercial insurance solutions.

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.