Tax-Advantaged Insurance Strategies for High Earners in California

How California high earners can leverage insurance for tax advantages including health insurance deductions, HSA strategies, tax-free wealth transfer, and estate planning.

INSURANCE TIPS

Felix | Pinoy General Insurance Services

3/30/202612 min read

You're earning $250,000+ annually. Between federal taxes, California state taxes, and FICA, you're losing 40-50% of every dollar to taxes.

But while you're diligent about maxing out your 401(k) and tracking deductions, you're likely missing significant tax advantages hidden in insurance strategies.

Here's what most high earners don't realize:

Self-employed health insurance can save you $15,000-$30,000/year

HSA strategies can create $500,000+ in tax-free retirement wealth

Life insurance can transfer millions tax-free to heirs

Long-term care premiums offer substantial deductions

Premium financing can leverage estate planning

After helping affluent Orange County residents optimize their insurance and tax strategies since 1993, I can show you exactly how to use insurance not just for protection—but as powerful tax-advantaged wealth-building tools.

This guide breaks down five tax-advantaged insurance strategies specifically for California high earners, with real examples, tax savings calculations, and implementation steps.

Strategy #1: Self-Employed Health Insurance Deduction

If you're self-employed, health insurance premiums are one of the most overlooked and most valuable tax deductions available.

Who Qualifies:

✅ Self-employed individuals (sole proprietors, partners, LLC members, S-corp shareholders with 2%+ ownership) ✅ Have net self-employment income ✅ Not eligible for employer-sponsored health insurance (through your employer or spouse's employer) ✅ Pay health insurance premiums for yourself, spouse, and dependents

What's Deductible:

Premiums for:

Medical insurance

Dental insurance

Vision insurance

Qualified long-term care insurance (with age-based limits)

Medicare premiums (Part B, Part D, Medicare Advantage, Medigap)

Where to Deduct:

Line 17 of Schedule 1 (Form 1040) - "above the line" deduction

Why this matters:

Reduces your Adjusted Gross Income (AGI)

Not subject to 7.5% AGI threshold like medical expense deductions

Reduces both federal AND California state income taxes

Also reduces self-employment tax calculation base

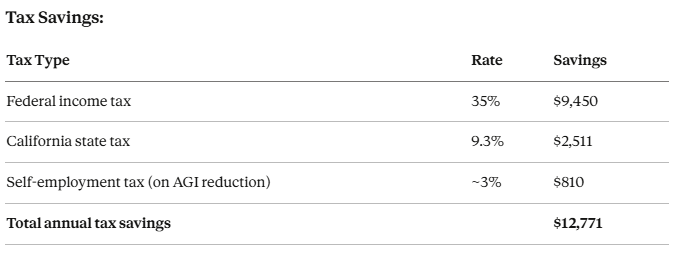

The Math - Real California Example:

Self-employed consultant earning $300,000/year

Health insurance premiums:

Family coverage: $24,000/year

Dental: $2,400/year

Vision: $600/year

Total premiums: $27,000/year

Effective cost of insurance: $27,000 - $12,771 = $14,229

You're getting $27,000 in health insurance for an effective cost of $14,229—a 47% discount via tax savings.

Over 20 years: $255,420 in tax savings (assuming consistent premiums and rates)

Common Mistakes:

❌ Mistake #1: Taking deduction when eligible for spouse's employer coverage

If you CAN get on spouse's plan, you can't take self-employed deduction

Strategy: Evaluate if tax savings outweigh spouse's employer contribution

❌ Mistake #2: Not deducting qualified long-term care premiums

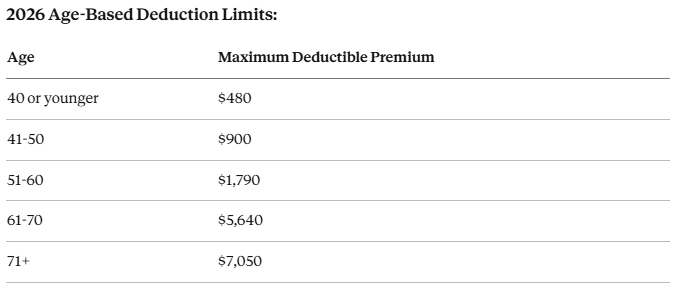

Age-based limits apply, but significant deductions available

Age 61-70: $5,640 deductible per person (2026 limits)

Often overlooked addition to health insurance deduction

❌ Mistake #3: S-Corp owners taking deduction incorrectly

Must include premiums in W-2 wages

Special reporting requirements

Consult tax professional for proper treatment

How to Maximize:

Step 1: Ensure you're truly self-employed and not eligible for employer coverage

Step 2: Document all health insurance premiums paid

Medical, dental, vision

Qualified long-term care

Medicare premiums (if applicable)

Step 3: Calculate deduction limit

Cannot exceed net self-employment income

If income is $50K but premiums are $30K, you can deduct full $30K

If income is $20K but premiums are $30K, deduction limited to $20K

Step 4: Report correctly on tax return

Schedule 1, Line 17

Also adjust self-employment tax calculation on Schedule SE

Step 5: Maintain documentation

Premium payment receipts

Policy documents

Proof of self-employment income

Related Reading: For more on business insurance fundamentals, see our complete guide.

Strategy #2: HSA Maximization for Tax-Free Wealth Building

Health Savings Accounts (HSAs) are the most tax-advantaged accounts available—better than 401(k)s, IRAs, or Roth IRAs for those who qualify.

The Triple Tax Advantage:

Contributions are tax-deductible (federal and California)

Growth is tax-free (no taxes on investment gains)

Withdrawals are tax-free (for qualified medical expenses)

No other account offers all three benefits.

Who Qualifies:

✅ Enrolled in High-Deductible Health Plan (HDHP) ✅ Not enrolled in Medicare ✅ Not claimed as dependent on someone else's taxes ✅ No other non-HDHP coverage (with some exceptions)

2026 Contribution Limits:

Individual coverage: $4,300

Family coverage: $8,550

Age 55+ catch-up: Additional $1,000

The High Earner Strategy: HSA as Stealth Retirement Account

Most people use HSAs wrong—they withdraw for current medical expenses. High earners should use HSAs as long-term wealth-building vehicles.

The Optimal Approach:

Step 1: Max out HSA contributions every year

Step 2: Pay current medical expenses OUT OF POCKET (don't withdraw from HSA)

Step 3: Invest HSA funds aggressively (stocks, index funds)

Step 4: Let HSA grow tax-free for decades

Step 5: After age 65, withdraw tax-free for:

Medicare premiums

Long-term care expenses

Any other qualified medical expenses

OR withdraw for any purpose (taxed as ordinary income, like traditional IRA)

The Math - Real Example:

California high earner, age 45, maxing family HSA for 20 years

Annual contribution: $8,550 Years contributing: 20 years (age 45-65) Total contributions: $171,000 Average annual return: 8% Account value at age 65: $415,869

Tax savings on contributions:

Federal (35% bracket): $59,850

California (9.3%): $15,903

Total tax savings: $75,753

At age 65-95 (30 years of retirement):

Medical expenses paid from HSA: $415,869

All withdrawals: 100% tax-free

If these were paid from taxable accounts: ~$166,000 in taxes (40% tax rate)

Total tax savings over lifetime: $241,753

From $171,000 in contributions, you've created $415,869 in tax-free wealth—a 143% increase solely from tax advantages and tax-free growth.

Advanced HSA Strategy: Triple-Dipping

Step 1: Pay medical expenses out-of-pocket during working years

Step 2: Save all receipts for these expenses (no time limit on reimbursement)

Step 3: Let HSA investments grow for 20-30 years

Step 4: In retirement, reimburse yourself for decades of saved receipts

Withdraw tax-free from HSA

Reimburse for expenses paid 20+ years ago

Use cash for any purpose (already reimbursed from HSA)

This converts HSA into tax-free cash with no restrictions.

Example:

Age 45-65: Pay $100,000 in medical expenses out-of-pocket, save receipts

Age 65: HSA worth $400,000

Withdraw $100,000 tax-free to "reimburse" 20-year-old expenses

Spend $100,000 on vacation, home renovation, grandkids—anything

Still have $300,000 in HSA for future medical needs

HSA Investment Allocation for High Earners:

Ages 40-55: 80-90% stocks (long time horizon) Ages 55-65: 60-70% stocks (still long-term, but approaching retirement) Ages 65+: 40-50% stocks (using funds over 20-30 year retirement)

Mistake to Avoid:

❌ Keeping HSA in cash/money market

You lose decades of tax-free growth

HSA is retirement account, not emergency fund

For more on maximizing insurance deductions, see our guide on homeowners insurance deductibles.

Strategy #3: Life Insurance as Tax-Free Wealth Transfer

For California high earners with estates exceeding federal estate tax exemption ($13.99 million in 2026, potentially dropping to ~$7 million in 2026), life insurance offers powerful tax-free wealth transfer.

Why Life Insurance for Estate Planning:

✅ Death benefit is income tax-free to beneficiaries ✅ Can be estate tax-free if properly structured (Irrevocable Life Insurance Trust) ✅ No probate (passes directly to beneficiaries) ✅ Creditor protection in California ✅ Guaranteed liquidity to pay estate taxes ✅ Cash value growth is tax-deferred (permanent policies)

The Estate Tax Problem:

California couple with $20 million estate

Federal estate tax (2026):

Exemption: $13.99 million (married couple)

Taxable estate: $6.01 million

Estate tax rate: 40%

Federal estate tax due: $2,404,000

Without liquidity, heirs forced to:

Sell family business

Liquidate investments at bad time

Sell real estate quickly (below market value)

Life Insurance Solution:

Purchase $3 million second-to-die life insurance policy:

Owned by Irrevocable Life Insurance Trust (ILIT)

Premium: ~$30,000-$50,000/year (depending on age/health)

Death benefit: $3,000,000 (income tax-free, estate tax-free)

Heirs use proceeds to pay $2.4M estate tax

Keep all assets intact

Cost over 20 years: $600,000-$1,000,000 in premiums Benefit: $3,000,000 tax-free to heirs Net gain: $2,000,000-$2,400,000

Types of Life Insurance for Wealth Transfer:

1. Second-to-Die (Survivorship) Life Insurance

How it works:

Insures two lives (typically spouses)

Pays death benefit after second death

Lower premiums than two individual policies

Best for:

Married couples with estate tax concerns

Estate exceeds federal exemption

Want to maximize death benefit per premium dollar

2. Whole Life Insurance

Features:

Guaranteed death benefit

Guaranteed cash value growth

Fixed premiums (never increase)

Dividends (from mutual companies)

Best for:

Want certainty and guarantees

Conservative investors

Willing to pay higher premiums for safety

3. Indexed Universal Life (IUL)

Features:

Death benefit protection

Cash value linked to stock index (S&P 500)

Downside protection (0% floor, no losses)

Upside potential (typically capped at 10-12%)

Flexible premiums

Best for:

Want growth potential without risk

Comfortable with caps on gains

Want premium flexibility

4. Variable Universal Life (VUL)

Features:

Death benefit protection

Cash value invested in sub-accounts (like mutual funds)

Full market exposure (risk and reward)

Flexible premiums

Best for:

Sophisticated investors

Want maximum growth potential

Comfortable with investment risk

Long time horizon (20+ years)

The Tax-Free Wealth Transfer Math:

High earner, age 50, $15 million estate

Option 1: No Planning

Estate tax at death: $2.4 million

Heirs receive: $12.6 million (net)

Option 2: $3M Life Insurance in ILIT

Annual premium: $40,000

Pay for 20 years: $800,000

Estate tax: $2.4 million

Life insurance proceeds: $3 million

Heirs receive: $15 million + ($3M - $2.4M) = $15.6 million net

Heirs get $3 million MORE than Option 1, despite $800K in premiums.

Advanced Strategy: Premium Financing

For very high net worth individuals, premium financing can magnify leverage:

How it works:

Take loan from bank/specialty lender to pay life insurance premiums

Collateralize with investments (don't liquidate)

Pay loan interest (deductible if structured properly)

At death, insurance pays loan and remainder to heirs

Example:

$10 million life insurance policy

Annual premium: $200,000

Borrow premiums for 10 years: $2 million

Pay loan interest: 5% = $100,000/year

At death: $10M pays off $2M loan, heirs get $8M

Total out-of-pocket: $1 million (interest) Heirs receive: $8 million net Effective cost: 12.5% of death benefit

For more on life insurance basics, see our life insurance guide for young families.

Strategy #4: Long-Term Care Insurance Tax Benefits

Long-term care (LTC) insurance offers significant tax advantages that most high earners overlook.

Federal Tax Benefits:

Premiums are tax-deductible as medical expenses (subject to 7.5% AGI threshold for itemizers)

For couples both age 65: $11,280 deductible ($5,640 × 2)

California Specific:

California allows the same deductions as federal, PLUS:

California Partnership Program:

Purchase qualifying LTC policy

Get "asset protection" equal to benefits received

If you need Medi-Cal later, protected assets don't count

Example:

Purchase LTC policy with $300,000 in benefits

Use $200,000 for care

$200,000 of your assets now protected if applying for Medi-Cal

Can keep additional $200K + normal Medi-Cal exemptions

The Tax Math for High Earners:

California couple, both age 65, $400,000+ AGI

LTC premiums paid:

His premium: $4,200/year

Her premium: $3,800/year

Total: $8,000/year

Tax deduction:

Maximum deductible (age 61-70): $5,640 each

Total deductible amount: $11,280

Exceeds actual premiums, so deduct full $8,000

But wait - 7.5% AGI threshold applies:

AGI: $400,000

7.5% threshold: $30,000

Must exceed $30,000 in medical expenses to deduct

Strategy: Bundle medical expenses

LTC premiums: $8,000

Health insurance (if self-employed): $20,000

Dental work: $5,000

Vision: $1,000

Total medical: $34,000

Deductible amount: $34,000 - $30,000 = $4,000

Tax savings:

Federal (35%): $1,400

California (9.3%): $372

Total: $1,772/year

Over 20 years: $35,440 in tax savings

Better Strategy for Business Owners:

If you own a C-Corporation:

Corporation pays LTC premiums as employee benefit

100% deductible to corporation (no AGI threshold)

Not taxable to you as employee

Benefits received are tax-free

Tax savings for C-Corp paying $8,000 in LTC premiums:

Corporate tax deduction (21%): $1,680

You avoid income tax on $8,000 benefit: $3,544 (44.3% combined CA+Federal)

Total annual tax savings: $5,224

Over 20 years: $104,480 in tax savings

For self-employed: LTC premiums qualify for self-employed health insurance deduction (Strategy #1), avoiding the 7.5% AGI threshold entirely.

Hybrid LTC Policies:

Consider life insurance with LTC rider:

Death benefit if you never need LTC

LTC benefits if you do need care

Premium may be fully deductible under self-employed health insurance deduction

Guarantees money isn't "wasted" if you don't use LTC

For more on protecting your business, see our key person insurance guide.

Strategy #5: Premium Financing for Estate Planning

Premium financing is an advanced strategy for ultra-high-net-worth individuals (estates $20M+).

How It Works:

Traditional approach:

Pay $200,000/year in life insurance premiums from cash flow

After-tax dollars (already paid income tax on this money)

Reduces investable assets

Premium financing approach:

Borrow from bank to pay premiums

Collateralize loan with securities (don't sell investments)

Pay only loan interest annually (5-7% typically)

Investments continue growing in your portfolio

At death, insurance pays loan + remainder to heirs

The Math - Real Example:

Age 60, $30M estate, needs $10M life insurance

Traditional Approach:

Annual premium: $300,000

Pay from cash flow for 10 years

Total out-of-pocket: $3,000,000

This money could have been invested elsewhere

Premium Financing Approach:

Borrow $300,000/year for 10 years: $3,000,000 total

Collateral: $3.5M in securities (don't liquidate)

Interest rate: 6%

Annual interest: ~$180,000 (averaged over 10 years)

Total interest paid: $1,800,000

At death:

Insurance pays: $10,000,000

Loan repayment: $3,000,000

Net to heirs: $7,000,000

Comparison:

Traditional: $3M in premiums, heirs get $10M

Financing: $1.8M in interest, heirs get $7M

But here's the key: The $3M in collateral securities that weren't liquidated:

Continued growing during 10 years at 8%: Now worth $6.5M

Plus generated income: $900,000

Total preservation: $7.4M

Net result:

Heirs get: $7M (insurance) + $6.5M (preserved securities) = $13.5M

Total cost: $1.8M (interest only)

Compare to traditional: $10M (insurance) + $0 (securities were liquidated for premiums)

Premium financing nets heirs $3.5M MORE.

Tax Advantages:

Interest may be tax-deductible if:

Structured as investment interest

Securities generate investment income

Subject to investment interest deduction limits

Strategy optimization:

Use dividend-paying stocks as collateral

Dividends cover part/all of interest payments

Potentially deductible interest reduces effective cost

Risks to Consider:

⚠️ Loan can be called if collateral value drops significantly ⚠️ Interest rates can rise (use rate caps/collars) ⚠️ Policy performance matters (especially with VUL/IUL) ⚠️ Regulatory changes could impact strategy

Best for:

Estates $20M+

Significant investable assets (to collateralize)

Long-term time horizon (10+ years)

Estate tax concerns

Want to preserve liquidity

For comprehensive business insurance planning, see our business insurance 101 guide.

Combining Strategies: The High Earner's Complete Tax-Advantaged Insurance Plan

Most powerful approach: Use ALL five strategies together.

Real California Example:

Self-employed professional, age 50, $500K income, $15M estate

Strategy 1: Self-Employed Health Insurance

Premium: $30,000/year

Tax savings: $13,000/year

Strategy 2: Max HSA

Contribution: $8,550/year

Tax savings: $3,850/year

Future value (20 years): $415,869 (all tax-free)

Strategy 3: Life Insurance in ILIT

$5M second-to-die policy

Premium: $60,000/year

Estate tax savings: $2,000,000 (for heirs)

Strategy 4: LTC Insurance

Premium: $8,000/year (both spouses)

Tax savings: $3,400/year (via self-employed deduction)

Strategy 5: Premium Financing (for portion of life insurance)

Finance $30,000 of $60,000 annual premium

Interest: $1,800/year

Preserves: $600,000 in investments over 20 years

Total Annual Out-of-Pocket:

Health insurance: $30,000 - $13,000 tax savings = $17,000

HSA: $8,550 - $3,850 tax savings = $4,700

Life insurance: $30,000 (self-paid) + $1,800 (financing interest) = $31,800

LTC: $8,000 - $3,400 tax savings = $4,600

Total: $58,100/year

Total Annual Benefits:

Insurance coverage: $5M+ in life insurance, comprehensive health, LTC protection

Current tax savings: $23,650/year

Future tax-free wealth: $415,869 (HSA) + preserved investments

Estate tax savings for heirs: $2,000,000+

Return on Investment:

Spending: $58,100/year

Current tax savings: $23,650/year

Net cost: $34,450/year

Protection + future wealth created: $7,000,000+

This is comprehensive tax-advantaged protection and wealth transfer.

Implementation Checklist

Quarter 1 (Now - March 31):

✅ Review current tax bracket and AGI ✅ Determine which strategies apply to your situation ✅ Gather current insurance policies for review ✅ Calculate potential tax savings from each strategy ✅ Consult with tax advisor on strategy implementation

Quarter 2 (April - June):

✅ If self-employed: Ensure health insurance deduction on tax return ✅ Open HSA (if eligible) and max contribution ✅ Get life insurance quotes for estate planning needs ✅ Evaluate LTC insurance options and tax benefits ✅ If ultra-high-net-worth: Explore premium financing

Quarter 3 (July - September):

✅ Implement chosen life insurance strategy (ILIT setup if needed) ✅ Review HSA investment allocation ✅ Purchase LTC insurance if appropriate ✅ Set up premium financing (if applicable) ✅ Document all strategies for year-end tax planning

Quarter 4 (October - December):

✅ Ensure all deductible premiums paid before 12/31 ✅ Max HSA contribution before year-end ✅ Review total tax savings achieved ✅ Plan next year's contributions and premiums ✅ Coordinate with CPA for tax return preparation

Common Mistakes High Earners Make

Mistake #1: Not Planning Because "Taxes Are Complicated"

Complexity is not an excuse to leave money on the table. These strategies can save $20,000-$50,000+ annually in taxes.

Mistake #2: Waiting Until Retirement to Use HSA

HSA should be your LAST account tapped in retirement, not your first. Use taxable accounts first, then tax-deferred, then HSA last for maximum tax efficiency.

Mistake #3: Buying Wrong Life Insurance Type

Term insurance is cheap but expires. For estate planning, you need permanent insurance that's guaranteed to pay out. Match policy type to goal.

Mistake #4: Not Using ILIT for Life Insurance

Life insurance owned by you is included in your taxable estate. ILIT removes it from estate, saving 40% in estate taxes on death benefit.

Mistake #5: Ignoring Long-Term Care Planning

One spouse's long-term care costs can devastate finances for surviving spouse. LTC insurance with tax benefits is crucial planning tool.

Working with Professionals

These strategies require coordination between:

Insurance Professional (us!):

Analyze coverage needs

Compare policy options

Structure for tax efficiency

Implement strategies

Tax Advisor/CPA:

Calculate tax savings

Ensure proper deductions

Integrate with overall tax strategy

Maximize benefits

Estate Planning Attorney:

Create ILIT (if needed)

Structure estate plan

Coordinate with insurance/tax strategies

Ensure legal compliance

Financial Advisor:

Integrate insurance with overall financial plan

HSA investment allocation

Premium financing evaluation

Wealth transfer coordination

We coordinate with all professionals to ensure seamless implementation.

Related Resources

For more information on insurance strategies, see our comprehensive guides:

Business Insurance 101 - Essential coverage for California small businesses

Key Person Insurance - Protecting your business from loss of critical employees

Life Insurance Guide for Young Families - Foundation life insurance planning

Homeowners Insurance Deductibles - Optimizing your deductibles for tax efficiency

Commercial Auto Insurance - Tax-deductible business vehicle coverage

Condo Insurance vs HOA Master Policy - Understanding coverage for condo owners

Flood Insurance in California - Protecting high-value properties

Get Your Free Tax-Advantaged Insurance Analysis

If you're a California high earner, you're likely missing significant tax savings through insurance strategies. But implementing these strategies requires expertise in both insurance and tax planning.

Contact Pinoy General Insurance Services for:

Free high-earner insurance analysis

Tax savings calculation for your situation

Strategy implementation roadmap

Coordination with your tax advisor and estate attorney

Annual review and optimization

Located at 17304 Norwalk Blvd, Cerritos, CA 90703, we've been helping affluent Orange County residents optimize their insurance and tax strategies since 1993. As a founding member of the Artesia Chamber of Commerce, we specialize in working with successful business owners and high-income professionals.

We specialize in tax-advantaged insurance for:

Self-employed professionals ($200K+ income)

Business owners

High-net-worth families (estates $5M+)

Ultra-high-net-worth (estates $20M+)

Anyone in 32%+ federal tax bracket

Call (562) 402-1737 or email info@pinoygeneralinsurance.com for your free tax-advantaged insurance analysis.

Don't leave $20,000-$50,000+ in annual tax savings on the table. Let us show you how insurance can be your most powerful tax-advantaged wealth-building tool.

About the Author:

Felix Lopez is a licensed insurance agent and business development manager at Pinoy General Insurance Services in Cerritos, California. Since 1993, Pinoy General Insurance has been helping Orange County's affluent residents and business owners leverage insurance for tax advantages, wealth transfer, and estate planning. Felix specializes in working with high-income earners to implement sophisticated insurance strategies that minimize taxes and maximize wealth preservation. He works closely with clients' CPAs, financial advisors, and estate planning attorneys to ensure seamless coordination of all financial strategies.

Pinoy General Insurance Services

17304 Norwalk Blvd

Cerritos, CA 90703

Phone: (562) 402-1737

Email: info@pinoygeneralinsurance.com

Website: pinoygeneralinsurance.com

Founding Member - Artesia Chamber of Commerce

Contact Us Today

Contact us here at Pinoy General Insurance Services today for all your insurance needs.

Phone

© 2025 Pinoy General Insurance Services. All rights reserved.